Oklahoma Sales Tax & Audit Guide

Straightforward Answers to Your Oklahoma Sales Tax Questions.

- Do I need to collect Oklahoma sales tax?

- Should I be collecting or paying Oklahoma use tax?

- What do I do if I should have been collecting but haven't?

- I received an audit notice. What should I do?

- Guidance on fighting a sales tax assessment in Oklahoma.

Who Needs to Collect Oklahoma Sales and Use Tax?

Like most states, to be subject to Oklahoma sales tax collection and its rules, your business must:

1) Have nexus with Oklahoma, and

2) Sell or use something subject to Oklahoma sales tax.

How is Nexus Established in Oklahoma?

According to the Oklahoma Department of Revenue, anyone engaged in business in Oklahoma must register with the Department of Revenue Services for a sales and use tax permit. A permit is required if you are selling tangible personal property on an ongoing basis.

"Tangible personal property" can be seen, weighed, measured, felt, or touched or in any other manner perceptible to the senses, including electricity, water, gas, steam, and prewritten computer software for frequent or occasional sales.

Any of the following establishes nexus:

(1) Maintenance of any business location in Oklahoma, including any kind of office.

(2) Ownership of real estate in Oklahoma.

(3) Ownership of a stock of goods in a public warehouse or on consignment in Oklahoma.

(4) Ownership of a stock of goods in the hands of a distributor or other non-employee representative in Oklahoma, if used to fill orders for the owner's account.

(5) Usual or frequent activity in Oklahoma by employee or representative soliciting orders with authority to accept them.

(6) Usual or frequent activity in Oklahoma by employee or representative engaged in a purchasing activity or the performance of services (including construction, installation, assembly, or repair of equipment).

(7) Operation of mobile stores in Oklahoma (such as trucks with driver-salespersons), regardless of frequency.

(8) Other miscellaneous activities by employees or representatives in Oklahoma such as credit investigations, collection of delinquent accounts, and conducting training classes or seminars for customer personnel in the operation, repair, and maintenance of its products.

(9) Leasing tangible property and licensing intangible rights for use in Oklahoma.

(10) The sale of other than tangible personal property such as real estate, services, and intangibles in Oklahoma.

(11) The performance of construction contracts or service contracts in Oklahoma.

Additionally, businesses that do not have a physical presence in Oklahoma can establish economic nexus by exceeding a certain annual sales threshold in Oklahoma.

Economic Nexus (Wayfair Law) and Internet Sales in Oklahoma Remote sellers have established economic nexus. They must register with the Department of Revenue to secure an Oklahoma Sales and Use Tax Permit if:

Sales of tangible personal property in Oklahoma of $100,000 or more during the preceding or current calendar year are required to collect and remit Oklahoma sales tax. The tax collection and remittance obligation will apply to the first calendar month following the month when the threshold is met.

For additional information, see Wayfair Law FAQ.

How is the $100,000 gross revenue threshold calculated?

All consideration for all sales is included in gross receipts subject to tax.

Marketplace Facilitators and Sellers

Marketplace facilitators must register with the Department of Revenue to secure a Sales and Use Tax Permit. A marketplace facilitator is any entity that:

- During the preceding twelve-month period, marketplace sellers facilitated retail sales of at least $250,000 by providing a forum to list or advertise a tangible personal property subject to sales and use taxes, including digital goods or taxable services.

- Collects receipts from customers and remits payments to the marketplace sellers

- either directly or indirectly, or through agreements with third parties; and

- Receives compensation or other consideration for provided services.

Marketplace Sellers

If your business sells through Amazon or a similar marketplace facilitator, you may not have to collect sales and use tax on those sales. Specifically, if the marketplace facilitator certifies that they collect and report sales tax on your sales, you are off the hook. However, such sales may still count towards your total sales threshold, meaning you’ll still need to collect tax on sales made directly through your website or any other marketplaces that don’t collect sales tax on your behalf.

Oklahoma Small Seller Exception

Oklahoma has a small seller exception, exempting certain sellers from remitting taxes for sales into Oklahoma. The exception applies to:

- a remote seller that had taxable sales of tangible personal property delivered to locations within this state worth less than $100,000 during the preceding or current calendar year

- a marketplace facilitator or a referrer that had taxable sales of tangible personal property delivered to locations within this state worth less than $10,000 during the immediately preceding twelve-calendar-month period

The small seller exception does not apply to sellers who have a physical presence in Oklahoma.

Which Sales are Subject to Oklahoma Sales Tax?

General Transactions

If you have nexus in Oklahoma, the next step is determining whether the products or services you sell are subject to Oklahoma sales and use tax.

Unless an item is specifically exempt, sales and rentals of tangible personal property are subject to Oklahoma sales tax.

The rules seem simple, but many details make applying Oklahoma’s tax rules to your business challenging. We recommend scheduling a time to review your specific situation with one of our sales tax professionals.

Common Exemptions from Oklahoma Sales and Use Tax:

Exempt items include:

- Medical Services

- Newspapers & Periodicals

- Utilities

- Fuel

- Raw Materials

- Machinery

Services

The Oklahoma Department of Revenue does not widely impose sales tax on services as long as the labor charges are separately stated from the purchase of materials on which the labor is performed.

For example, a business that provides alteration services on fur coats:

“Persons utilizing fur in the altering, repairing, or remodeling of furs for others are vendors of the fur used in connection with such altering, repairing, or remodeling and shall collect, report and remit the tax at the time the fur is sold.

The sales price of such fur shall be segregated on the bills or invoices to the customer from the charge for labor in connection with such altering, repairing, or remodeling. Failure to separate the sale of material from the cost for labor requires paying the tax on the entire amount charged to customers”. See Page 220 in Chapter 65 Sales and Use Tax 2021 (oklahoma.gov)

Another example is a business that provides installation services:

“Where the quoted or advertised price is a lump sum for both property and installation or where billing and other records do not show separate charges for property and installation, the measure of the tax is the total gross receipts received by the seller.

Where the seller has a standard retail sales price for his products and where the typical sales price is used both when making across-the-counter sales and when selling and installing the property, he may make a separate and additional charge for making the installation which, when shown separately in his billings and on his books, will not be subject to the sales tax.”

For more information see page 225 in Chapter 65 Sales and Use Tax 2021 (oklahoma.gov)

Software

Many people have questions about the taxability of Software as a Service (Saas).

Many states already impose a tax on software as a service. As these options proliferate, states are moving to update their tax laws and, naturally, impose a tax.

To determine whether you need to collect tax on software sales, we highly recommend contacting one of our sales tax professionals to help you sort it out.

That said, here is the information you need to determine the taxability status of your software products and services:

Definitions

- "Computer software" means a set of coded instructions designed to cause a "computer" or automatic data processing equipment to perform a task.

- "Computer software maintenance contract" means a contract that obligates a vendor of computer software to provide a customer with future updates or upgrades to computer software, support services concerning computer software, or both.

- "Electronic" refers to technology having electrical, digital, magnetic, wireless, optical, electromagnetic, or similar capabilities.

- "Load and leave" means delivery to the purchaser using tangible storage media where the tangible storage media is not physically transferred to the purchaser.

- "Prewritten computer software" means "computer software," including prewritten upgrades, which are not designed and developed by the author or other creator to the specifications of a specific purchaser. Prewritten software includes software designed and developed by the author or creator to the specifications of a particular purchaser when sold to a person other than the purchaser. Combining two or more prewritten computer software programs or prewritten portions does not cause the combination to be other than prewritten computer software.

- "Mandatory computer software maintenance contract" means a computer software maintenance contract that the customer is obligated by contract to purchase as a condition of the retail sale of computer software.

- "Optional computer maintenance contract" means a computer software maintenance contract that a customer is not obligated to purchase as a condition of the retail sale of computer software.

Taxability

- Sale or rental of a computer. The sale of a computer and its related components is subject to sales or use tax. The rental of a computer and its associated components, including terminal equipment (hardware), is subject to sales tax.

- Sale of prewritten computer software. The sale of prewritten computer software delivered in a tangible media format is taxable. Prewritten computer software delivered utilizing "load and leave" is also taxable.

- Maintenance contract sold with prewritten computer software. The taxability of a maintenance contract sold with prewritten computer software delivered in a tangible media format depends on whether the maintenance contract is mandatory or optional.

If the contract is mandatory, the total sale price, including the charge for the contract, is subject to tax.

- The charge for an optional contract shall be subject to taxation:

- If it provides only upgrades or updates which include prewritten computer software delivered in a tangible media format; or,

- If it provides both upgrades or updates and support services and the fee for the support services is not stated separately.

- If the contract is optional and provides only maintenance agreement support services, the contract is not taxable.

- Written training materials. Written training materials are taxable, although the training services themselves are not.

- Modifications to prewritten computer software. Modifications to "prewritten computer software" do not result in the production of custom computer software. Where a person modifies or enhances computer software of which the person is not the author or creator, the person shall be deemed to be the author or creator only of such person's modifications or enhancements. Prewritten software or a prewritten portion thereof that is modified or enhanced to any degree, where such improvement or enhancement is designed and developed to the specifications of a specific purchaser, remains prewritten software; provided, however, that where there is a reasonable, separately-stated charge or an invoice or other statement of the price is given to the purchaser for such modification or enhancement, such modification or enhancement shall not constitute prewritten computer software.

- Custom computer software. "Custom computer software" means a program prepared to particular customer specifications. The sale of a custom computer program is a service transaction and is not subject to tax. In addition, maintenance charges are not taxable.

- Software purchased with a computer. The charge for prewritten computer software purchased with a computer is subject to tax. If a computer is bought with custom software and the cost for the software is not separately stated, the entire purchase price is subject to tax. In addition, the total charge is subject to tax if modifications are required, the charge for the modifications is not separately stated, and records do not adequately document the extent of the modifications.

For more information, see page 203 in Chapter 65, Sales and Use Tax 2021 (oklahoma.gov)

Shipping & Handling

- Separately stated delivery charges. In every case where a delivery charge represents the cost of transporting the items sold from the vendor to the consumer and is separately stated on the invoice or statement, such charges are not subject to sales tax.

- Delivery charges are included in the price. If delivery charges are included in the selling price of the tangible personal property sold, the charges are subject to sales tax.

- Transportation costs of the seller. Shipping, freight, or delivery charges paid by a seller in acquiring property for sale are considered costs of doing business to the seller and may not be deducted from the gross proceeds of the sale in computing tax liability, even though such costs may be passed on to his customers and regardless of whether they are separately stated.

- Demurrage. Demurrage is a charge for detaining a ship, freight car, or truck beyond the time allowed for loading or unloading, is considered a penalty, and is not subject to sales tax.

For more details, see page 208 in Chapter 65, Sales and Use Tax 2021 (oklahoma.gov)

Industry-Specific Guidance

While the general sales tax rules seem straightforward, applying those rules can get tricky when gray areas arise. The Oklahoma Department of Revenue provides some specific guidance for vehicle sales tax and medical marijuana sales tax beginning on page 230 in Chapter 65, Sales and Use Tax 2021 (oklahoma.gov)

Determining Local Sales Tax Rates in Oklahoma

Oklahoma’s statewide sales tax rate is 4.5%. Four hundred sixty-nine local and special-purpose tax jurisdictions impose additional sales taxes in Oklahoma.

Local Sales and Use Tax Tables

Here you can look up local Oklahoma sales tax rates. Or find your city’s local tax rate in the chart below:

*Exact tax rates vary. Occupancy fees and taxes are not included in this table.

I Should Have Collected Oklahoma Sales Tax, But I Didn't

Many of our competitors will suggest filing a Voluntary Disclosure Agreement in each state. This is a one-size-fits-all solution that isn't always the best. Our sales tax professionals will work with you to determine your business's best and most cost-effective solution.

If you determine your business has nexus, but you have not collected Oklahoma sales tax, here are your options:

1. Register and pay back taxes, penalties, and interest, or

2. Complete a VDA to cut penalties (and, in some cases, reduce your tax liability and avoid interest).

Here is what you need to know about each option to make the best decision for your business:

Option 1: Register to Pay Back Taxes, Penalties, and Interest

A VDA is not cost-effective if the past liabilities and penalties are minimal. Sometimes the best resolution for a business is to register with Oklahoma and pay back taxes, penalties, and interest.

Be wary of the tax professionals recommending a VDA in these cases. They want to make a buck rather than look out for your best interests.

When to consider registration and payment:

- If you established nexus less than 3 or 4 years ago.

- The sales tax penalty is LESS than the professional fees charged for the VDA.

- Your business does NOT have a sales tax collected issue.

Beware: Registering does not generally end past liabilities.

If you're unsure what your past liabilities are, contact us. Our state tax professionals work with you so you can make the right choice for your business.

Option 2: Voluntary Disclosure Agreement (VDA)

Oklahoma's lookback period: The standard lookback period is three years.

In many situations, voluntary disclosures are a valuable tool to reduce extended periods of past exposure.

The voluntary disclosure limits the lookback period to three years. So, if you should have collected sales tax over the past ten years but didn't, you may benefit from doing a VDA.

A VDA may be a good option for you if:

- You established nexus more than 3 or 4 years ago.

- You have a sales tax collected but not remitted issue.

- The sales tax penalty savings is MORE than the professional fees charged for the VDA.

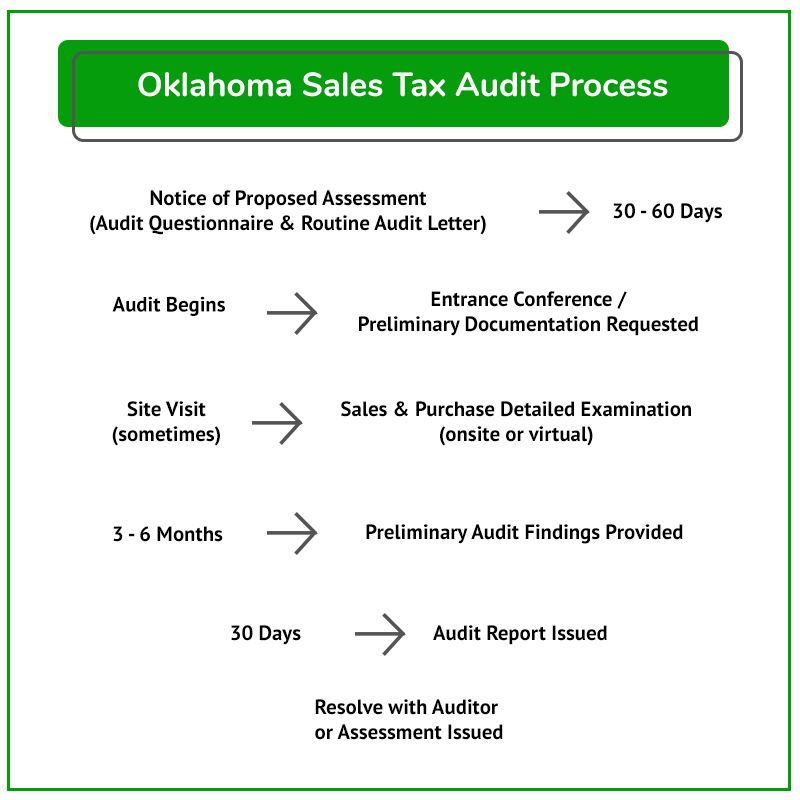

What to Expect During an Audit

The typical audit process is shown in this flowchart. Detailed guidance for each stage of the audit process follows in the sections below.

Oklahoma regularly audits businesses required to charge, collect, and remit various taxes in the state.

Many audits begin with a call from an Oklahoma Department of Revenue sales tax auditor.

Shortly after the call, your business will receive a Notification of Intent to Audit. This notification confirms that you were lucky enough to be chosen for an Oklahoma sales tax audit.

It is good to start with getting a state and local tax professional involved to prepare for the audit.

I Received an Oklahoma Sales Tax Audit Notice. What Should I Do?

Businesses that receive a sales tax audit notice need to consider the following questions:

- If you don’t have sales tax audit experience, how can you trust that the state's auditor abides by the rules and follows proper procedures?

- How will you know when to provide documents or when to push back?

- Do you thoroughly understand your sales and use tax areas of exposure?

- Controlling the audit is paramount to limiting exposure and shaping the results. Are you confident in doing that on your own?

Unless you can confidently answer these questions, hiring a professional is most likely to be the best option.

Contact us to learn how our sales tax professionals can give you the peace of mind and confidence you’ll need during your audit.

Visit our resource pages for more information to help you make critical decisions during your Oklahoma sales and use tax audit.

The Audit Overview & Selection Process

Statute of Limitations Extensions & Issues

Managing the Sales Tax Auditor

What to Expect from an Oklahoma Sales Tax Auditor

You can read through this Oklahoma Department of Revenue Field Audit Guide for more detailed information, but for now, here is a summary of the general audit process:

- The auditor will conduct pre-audit research.

- The auditor will often schedule and perform an entrance conference.

- The auditor will request records (many of which the auditor is not entitled to and does not need)

Once the auditor receives the necessary records, they will compare your Oklahoma sales and use tax returns to your federal income tax returns or bank statements to determine whether you reported all applicable or gross sales on your Oklahoma sales tax return(s).

NOTE: A slight error in how the tax was charged on even a single type of transaction can add up to a significant sales tax liability.

Once the auditor is confident all sales are accounted for, they will:

- Review your exempt and out-of-state sales.

- Conduct a use tax audit – the auditor will request accounts documents to make sure you paid use tax adequately on applicable purchases.

Common areas audited include:

- Advertising Expense

- Auto & Truck Expense

- Repair and Maintenance

- Office Expense

- Miscellaneous Expense

- Supplies

- Equipment

If a business buys an item online without paying use tax, the business is still obligated to remit the tax to Oklahoma. Believing otherwise often leads to shocking results for the unsuspecting taxpayer during an audit. Here is more information on Oklahoma Use Tax.

If you have questions about your situation, contact us to discuss it with one of our tax professionals.

After the Audit – Understand and Defend Your Businesses Rights

Upon completion of the audit, there will usually be an exit conference with the auditor. The auditor will produce an audit report with corresponding work papers to support the Oklahoma sales and use tax assessment.

It is advisable to have a sales tax professional present during this meeting. This is your first opportunity to see the auditor's findings. You'll want to push back on areas where they have overstepped their bounds or misapplied Oklahoma's sales tax laws.

It's best to hold off on agreeing to the sales tax assessment until a sales tax professional has reviewed it for issues that should be challenged.

| Many businesses wind up drastically overpaying the state because the business owner or in-house accounting personnel weren't well versed in the sales tax laws that, if challenged, could have reduced their sales tax liability. |

We'll cover the process of challenging an Oklahoma sales tax audit assessment in detail in the following sections.

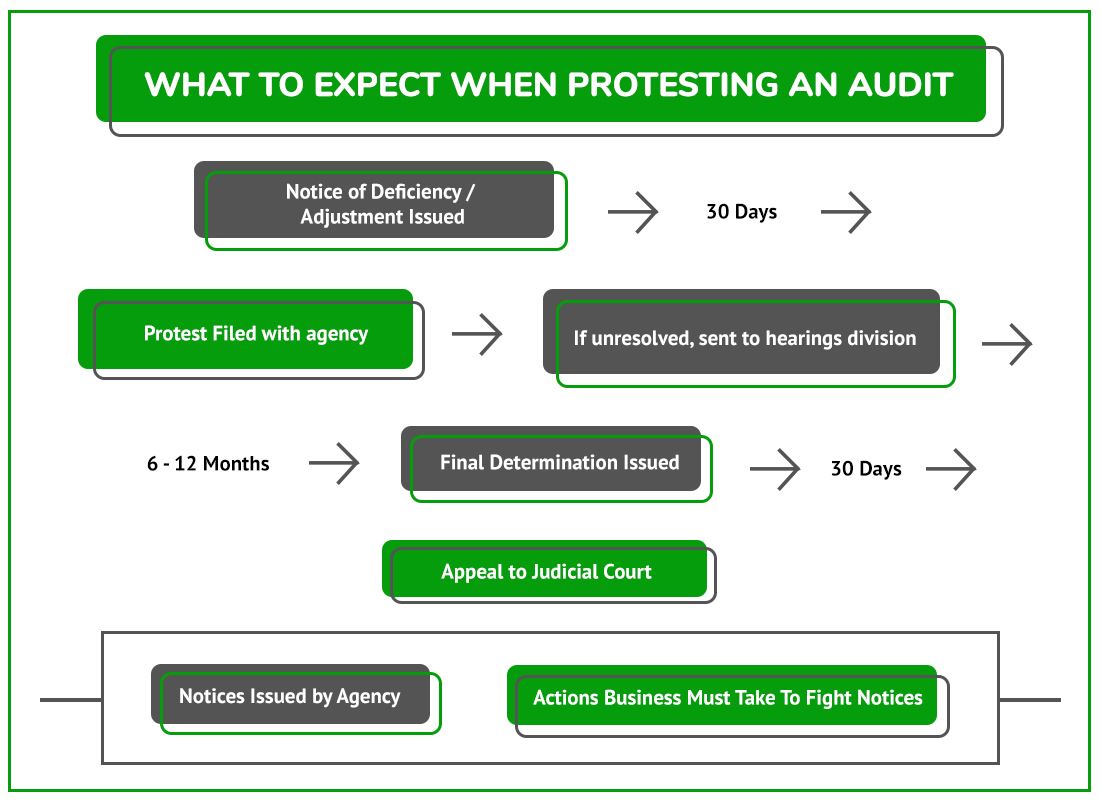

Contesting Audit Findings with the Auditor

Oklahoma Sales Tax Audit Protest Process Flow Chart

NOTE: If the deadlines are missed, it can be tough to get the case reopened.

After an audit, the auditor will issue a Tax Determination Report (AKA the audit report). It's essential to review and understand its implications carefully.

The audit report:

- Details of the auditor's findings

- Describes any proposed audit adjustments

- Shows the amount of tax, interest, and penalty due

If you disagree with the proposed changes, you may request an informal conference with the auditor. You must request an informal conference and attempt to resolve the case with the auditor.

Audit Closing Conference

The taxpayer has a short period to contest the findings with the auditor. Any issues with the results are handled as follows:

1. Issues related to exemptions, proof of tax paid, and calculations are worth addressing with the auditor.

2. Legal interpretations of sales tax law are often not resolvable at this stage.

After this conference, the auditor will adjust the audit assessment, and a notice of assessment will be issued.

Suppose you cannot resolve this with the auditor. In that case, the next step is to appeal/protest the issue with the Oklahoma Office of the Administrative Law Judge.

Appeal/Protest with The Oklahoma Department of Revenue

You’ll have the following options within 60 days of the assessment:

- Request an extension of up to an additional 90 days to go over the findings and submit additional records for review

- Request consideration for waiver of penalty and interest, which requires tax to be paid in full

- Request a payment plan

- Protest the review

- Settle your tax liability

Protest Rights and Audit Finding Confirmation

- If you disagree with an audit's findings, you must file an appeal 60 days from the first formal billing / Notice of Assessment date.

- The appeal must state why the assessment, the tax, interest, or penalties are incorrect.

- You must complete a protest/appeal within 60 days, sixty (60) days from the first formal billing notice date.

If you have received a Notice of Assessment and haven't talked to someone experienced in Oklahoma State tax, now is the time. Do it before these deadlines are missed.

Final Decision

If a hearing before the Administrative Law Judge is requested and granted, the Administrative Law Judge will submit recommendations to the Tax Commission. The Tax Commission will make a final determination before scheduling the hearing.

If the assessment is not settled to your satisfaction by the Administrative Law Judge, you’ll have thirty (30) days from the date of mailing of the order to appeal to the Oklahoma Supreme Court directly.

Our team has handled hundreds of administrative court cases. It can help your company receive the resolution you are entitled to. Get in touch with us today.

Settling an Oklahoma Sales Tax Liability

After any critical notices are issued, settling your Oklahoma sales tax case with the Oklahoma Department of Revenue is possible by filing an Oklahoma Offer in Compromise. The business must meet specific criteria to qualify, but you can get better results negotiating here than with the auditor. However, knowing a fair settlement from an unreasonable settlement will be challenging without experience and knowledge of Oklahoma tax laws.

DO NOT attempt to negotiate a settlement without an experienced Oklahoma state and local tax lawyer or other professional.

Contest an Oklahoma Jeopardy Assessment

Oklahoma may issue a Notice of Jeopardy Determination in certain situations.

The jeopardy assessment gives the Oklahoma Department of Revenue the right to try to collect immediately.

Due to the jeopardy nature, the taxpayer only has a very short time to contest the assessment and must place a security deposit to fight the issue.

Oklahoma Supreme Court

Other Oklahoma Sales Tax Resources

Oklahoma Department of Revenue Sales Tax Website

Chapter 65 - Oklahoma Sales and Use Tax

Oklahoma Tax Commission Business Help Center

Do You Need to Collect Oklahoma Sales Tax?

If you have received a Notice of Assessment and haven't talked to someone experienced in Oklahoma State tax, now is the time. Do it before these deadlines are missed.

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.