New Mexico Sales Tax & Audit Guide

Straightforward Answers to Your New Mexico Sales Tax Questions.

- Do I need to collect New Mexico sales tax?

- Should I be collecting or paying New Mexico use tax?

- What do I do if I should have been collecting but haven't?

- I received an audit notice. What should I do?

- Guidance on fighting a sales tax assessment in New Mexico.

Who Needs to Collect New Mexico Sales and Use Tax?

New Mexico is among the few states with a gross receipts tax structure instead of a sales tax. The gross receipts tax, very different from a sales tax, is a tax on the privilege of doing business in this state. It applies to the total amount of money or other considerations (barter, for instance) that a business receives for its transactions here in New Mexico.

The Gross Receipts Tax rate throughout the state varies from 5.125% to 9.4375%. It is a combination of rates imposed by the state, counties, and municipalities where the businesses are located.

Businesses must use the location code and tax rate corresponding to where their goods or the product of their services are delivered.

Gross receipts are the total amount of money, value and other considerations, including:

- Selling a New Mexico property.

- Leasing or licensing property in New Mexico.

- Granting a right to use a franchise operated in New Mexico.

- Providing services in New Mexico and outside of New Mexico, the product of which is first used in New Mexico

- Selling research and development services from outside New Mexico, the product of which is first used in New Mexico.

How is Nexus Established in New Mexico?

Any person who engages in business in New Mexico must register with the Taxation and Revenue Department.

"Engaging in business" means doing or causing any activities for the purpose of direct or indirect benefit.

Additionally, businesses that do not have a physical presence in New Mexico can establish economic nexus by exceeding a certain annual sales threshold.

Economic Nexus (Wayfair Law) and Internet Sales in New Mexico

For a retailer who lacks a physical presence in this state, including a marketplace provider, "engaging in business" is defined as having, in the previous calendar year, total taxable gross receipts from all sales, leases, and licenses of tangible personal property, and sales of licenses and sales of services and licenses for the use of tangible property sourced to New Mexico totalling at least one hundred thousand dollars ($100,000).

How is the $100,000 gross revenue thresholds calculated?

Gross receipts are the total money and any other consideration received from the above activities. While the Gross Receipts Tax is imposed on businesses, it is commonly passed on to the purchaser by separately stating it on the invoice or combining the tax with the selling price.

Marketplace Facilitators and Sellers

- Marketplace facilitators with physical nexus in New Mexico must collect and remit sales and use tax.

- A marketplace facilitator without a physical nexus that reaches the $100,000 threshold in the current calendar year must begin collecting and remitting sales tax on or before the first day of the second calendar month after exceeding the threshold.

A marketplace seller is a seller that sells or offers tangible personal property or other products or services subject to New Mexico sales or use tax through a marketplace owned, operated, or controlled by a marketplace facilitator. If your business sells through Amazon or a similar marketplace facilitator, you may not have to collect sales tax on those sales.

Specifically, if the marketplace facilitator certifies that they collect and report sales tax on your sales, you are off the hook. However, such sales may still count towards your total sales threshold, meaning you’ll still need to collect tax on sales made directly through your website or any other marketplaces that don’t collect sales tax on your behalf.

Which Sales are Subject to New Mexico Sales Tax?

General Transactions

Taxes in New Mexico are on transactions and not on items. Five kinds of transactions are subject to the tax:

- Sale of property in New Mexico.

- Leasing or licensing property in New Mexico.

- Granting the right to use a franchise operated in New Mexico.

- Performance of services* in New Mexico, and

- Performance of services outside of New Mexico, the product of research and development services out of state when initial use of the product was initially used in New Mexico.

The law presumes that all transactions are taxable unless a statute provides an exemption or deduction. See FYI-105 for a listing of exemptions and deductions.

We recommend scheduling a time to review your specific situation with one of our sales tax professionals.

Common Exemptions from New Mexico Sales and Use Tax:

Gross receipts are taxable, exempt, or deductible. Those receipts are taxable if they do not fall under any exemption or deduction.

Exempt items include:

Agricultural Exemptions

- Growers, producers, and trappers sell livestock and unprocessed agricultural products (a bale of hay, a head of lettuce, or an unroasted sack of green chile).

- Exception: charges from selling dairy products at retail are not exempt.

- Receipts of persons feeding or pasturing livestock (7-9-19).

Athletic Facility Surcharge Exemption

- Receipts of a university from an athletic facility surcharge imposed under the University Athletic Facility Funding Act (7-9-41.1).

Disabled Street Vendor Exemption

- Sales of disabled street vendors (7-9-41.3).

Food Stamp Exemption

- Sales from the redemption of food stamps (7-9-18.1).

Fuel Exemptions

- Receipts from gasoline sales, special fuel, alternative fuel on which the gasoline, special fuel excise, or alternative fuel excise tax has been paid and not refunded (7-9-26).

- Receipts from selling a substance that combines fuel and oxidizer to propel space vehicles or to operate space vehicle launchers (7-9-26.1).

Governmental Entity Exemptions

- Sales to the federal government, State of New Mexico, or any Indian nation, tribe, or pueblo from transactions occurring on its sovereign territory, or any agency or political subdivision of the preceding; for example, cities, counties, and public schools. Foreign nations' receipt is exempt when the exemption is required by a treaty to which the United States is a party (7-9-13).

- Exception: receipts of state political subdivisions from operating a gas or electric utility or a municipal cable television system are not exempt.

- Sales of instrumentalities of the armed forces of the United States (7-9-31).

- Sales to Indian nations, tribes, pueblos, or their members, are exempt if the transaction takes place on the tribe's territory (see "Federal Preemption" on page 9).

Insurance Company and Bail Bondsman Exemption

- Receipts of insurance companies or their agents from premiums and receipts of property bondsmen from security for a bail bond (7-9-24).

Interest and Dividend Exemption

- Interest on money loaned; dividends or interest from stocks, bonds, or securities; and receipts from the sale of stocks, bonds, or securities (7-9-25).

Interstate Telecommunications Services Exemption

- Receipts from sales of interstate telecommunications services (7-9-38.1).

- NOTE: these services are subject to the interstate telecommunications gross receipts tax.

- Isolated and occasional sale exemption receipts from the solitary or occasional sale of or leasing of property or service by a person not in the business of selling or leasing the same or similar property or service (7-9-28).

Mobile telecommunications services exemption

- Charges of a home service provider from providing mobile telecommunications services to persons whose place of primary use is outside New Mexico, regardless of where the mobile telecommunications services originate, terminate, or pass through (7-9-38.2).

Municipal Event Center Surcharge Exemption

- Receipts from selling tickets, parking, souvenirs, concessions, programs, advertising, merchandise, corporate suites or boxes, broadcast revenues, and all other products or services sold at or related to a municipal event center or related to activities occurring at the event center on which an event center surcharge is imposed under the Municipal Event Center Funding Act (7-9-13.5).

Oil, Natural Gas, and Mineral Exemptions

- Oil, natural gas, or liquid hydrocarbons, individually or any combination thereof, carbon dioxide, helium, or a non-hydrocarbon gas subject to the Oil and Gas Emergency School Tax Act that are sold for resale, for consumption outside New Mexico, or use as an ingredient or part of a manufactured product (7-9-33).

- Receipts from the sale or the processing of products, the processing of which is subject to the Natural Gas Processors Tax Act, or for receipts from storing or using crude oil, natural gas, or liquid hydrocarbons by a processor or by a person engaged in the business of refining oil. (7-9-34).

- Exception: Receipts from the sale of products other than for subsequent resale in the ordinary course of business for consumption outside New Mexico or for use as an ingredient or part of the manufacturing product are subject to the Gross Receipts Compensating Tax Act and the Natural Gas Processors Tax Act.

- Natural resources subject to the Resources Excise Tax Act when they are sold for resale or an ingredient or part of a manufactured product (7-9-35).

- Charges from the sale or lease of oil, natural gas, or mineral interests (7-9-32).

- Receipts from the sale of oil, gas, or liquid hydrocarbons consumed as fuel in the pipeline transportation of such products (7-9-36).

Out-of-State Services Exemption

- Receipts from services performed outside the state when the product of the service is first used in New Mexico (7-9-13.1).

- Exception: receipts from performing a research and development service are not exempt unless the service is: sold between affiliated corporations; sold to the United States government by operators of national laboratories (other than 501(c)(3) organizations); or sold to persons (other than 501(c)(3) organizations) operating national laboratories.

Racetrack Exemption

- Receipts of horse riders, jockeys, and trainers from race purses at New Mexico horse racetracks and receipts of racetracks from gross amounts wagered.

School Event Services Exemption

- Receipts from umpiring, refereeing, scoring, or other officiating at school events sanctioned by the New Mexico Activities Association (7-9-41.4).

- Stadium Exemption

- Receipts from sales of tickets, souvenirs, parking, concessions, corporate suites or boxes, programs, advertising merchandise, broadcast revenues, and all other products, services, or activities sold at or related to a minor league baseball stadium where a stadium surcharge is imposed under the Minor League Baseball Stadium Funding Act (7-9-13.3).

Textbook Exemption

- Receipts of certain bookstores from selling textbooks and materials required for public post-secondary educational institution courses at a to a student enrolled at the institution (7-9-13.4).

- Requirement: bookstore must be located on the institution's campus and operated by contract with the institution.

- Requirement: a student must present valid student identification.

Vehicle, Boat, and Fuel Exemptions

- Receipts from selling vehicles are subject to the motor vehicle excise tax, and cars are exempt from the motor vehicle excise tax under Section 7-14-6 NMSA 1978 (7-9-22).

- Exception: the sales of manufactured homes are subject to tax.

- Receipts from selling boats are subject to the boat excise tax (7-9-22.1).

For more information about exemptions, deductions, and credits, see FYI-105 (newmexico.gov)

Services

'Professional services require a license from the state to perform or require a master's degree or better to perform, such as accounting services, architectural services, engineering services, information technology services, and legal services. Please see FYI 200 for information about choosing the correct location and tax rate for your receipts.

New Mexico does not impose a tax based on the point of delivery of the goods sold. Instead, New Mexico charges a tax on the gross receipts of the seller or lessor, the person engaging in business. The seller or lessor's business location determines the tax rate.

NOTE: As of July 1, 2019, a business that has had $100,000 in taxable gross receipts from sales/leases/licenses of tangible personal property or sales of services of real property that are sourced to New Mexico in the prior year is engaging in business, and gross receipts tax is due. Businesses with no physical locations in New Mexico will report gross receipts tax at the out-of-state rate of 5.125%.

Starting July 1, 2021, New Mexico will impose the gross receipts tax based on the location where the tangible personal property is delivered except as stated in statute or regulation.

Receipts from professional services may be deducted from gross or governmental receipts when the sale is made to a person engaged in the manufacturing business and provides a nontaxable transaction certificate to the seller. The services must be related to the product that the buyer is in the business of manufacturing.

Software

Information technology services are defined as: separately stated services for installing and maintaining a business's computers and computer network, including performing computer network design; installing, maintaining, repairing, or restoring computer networks, hardware, and software; performing custom software programming or making custom modifications to existing software programming.

"Information technology services" do not include:

- Data processing services or processing of information to compile and produce records of transactions for retrieval or use, including data entry, data retrieval, data searches, information compilation, or access to telecommunications or the internet.

Performed in a qualified area by an eligible software company (7-9-57.2).

- Software maintenance or update agreements unless they are made in conjunction with custom programming.

- Computers, servers, chilling equipment, and pre-programmed software.

Sales of software development services

- Requirement: Only a taxpayer whose primary business is in New Mexico and established after July 1, 2002, is eligible for this deduction.

- The seller must perform the software development services outside Albuquerque, Las Cruces, Santa Fe, and Rio Rancho municipal boundaries.

- Exception: This does not include software implementation or support services.

Shipping & Handling

Gross receipts tax generally applies to delivery and shipping charges, including postage and transportation charges, in New Mexico, whether the charges are separately stated or included in the sale price.

Industry-Specific Guidance

While the general sales tax rules seem straightforward, applying those rules can get tricky when gray areas arise. The New Mexico Taxation and Revenue Department provides some specific guidance for the following industries:

Determining Local Sales Tax Rates in New Mexico

The state rate of 5.125% is the base. Local option taxes are gross receipts taxes that counties and municipalities impose for their own revenues.

As a convenience, the state collects taxes for the local governments. It then redistributes the income to the county or municipality imposing the tax. The state collects local option taxes simultaneously and in the same manner as state gross receipts tax.

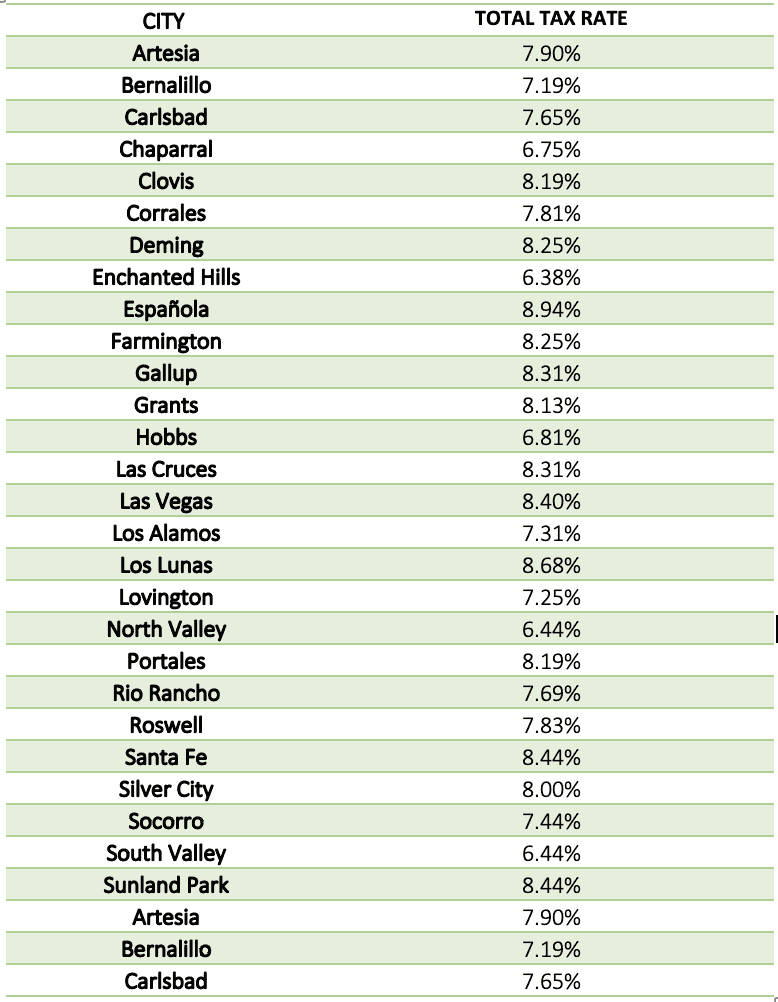

Local Sales and Use Tax Tables

Here you can look up local New Mexico sales tax rates. Or find your city’s local tax rate in the chart below:

*Exact tax rates vary. Occupancy fees and taxes are not included in this table.

I Should Have Collected New Mexico Sales Tax, But I Didn't

A managed audit allows retailers to conduct the audit on themselves as specified in a signed agreement between the Secretary and the taxpayer or the taxpayer's authorized representative.

The managed audit program allows a retailer to disclose tax due and avoid paying penalties and interest, as long as the assessment is paid within 180 days from the assessment date. When the assessment is not paid in full within 180 days, interest will be assessed on the remaining tax due from the time that tax was originally due until it is paid.

There are two options for conducting the managed audit:

Option A – You will prepare the audit work papers with minimum guidance from the Department. You will receive a written statement from the Department stating that you may remain subject to audit by the Department for the audit period.

Option B –You will work with an assigned auditor to develop an audit plan and provide all records required to complete the audit. After completion and acceptance of the audit, you will be issued a written statement from the Department stating that the specific issues in the audit period covered by the agreement are closed to further audit by the Department.

If you're unsure what your past liabilities are, contact us. Our state tax professionals work with you so you can make the right choice for your business.

What to Expect During an Audit

The typical audit process is shown in this flowchart. Detailed guidance for each New Mexico audit process stage follows in the sections below.

Notification of Intent to Audit. (Audit Questionnaire & Routine Audit Letter) -- --> 60 days Audit Begins --> Entrance conference/preliminary documentation requested --> Site Visit (sometimes) --> Sales & Purchase detailed examination (onsite or virtual)--> the Department will request outstanding records between 60 and 180 days after the beginning of the audit. If you do not produce the documents within 90 days, the Department can issue an assessment of tax based on the information as it stands --> -6 months --> preliminary audit findings provided --> 0 days audit report given --> 30 days --> Resolve with auditor or assessment issued.

New Mexico regularly audits businesses required to charge, collect, and remit various taxes in the state. Many audits begin with a call from a New Mexico Taxation and Revenue Department sales tax auditor. Shortly after the call, your business will receive a Notification of Intent to Audit. This notification confirms that you were lucky enough to be chosen for a New Mexico sales tax audit.

It is good to start with getting a state and local tax professional involved to prepare for the audit.

I received a New Mexico Sales Tax Audit Notice. What Should I Do?

Businesses that receive a sales tax audit notice need to consider the following questions:

- Suppose you don't have sales tax audit experience. How can you trust that the state's auditor abides by the rules and follows proper procedures?

- How will you know when to provide documents or when to push back?

- Do you thoroughly understand your sales and use tax areas of exposure?

- Controlling the audit is paramount to limiting exposure and shaping the results. Are you confident in doing that on your own?

Unless you can confidently answer these questions, hiring a professional is most likely to be the best option.

Contact us to learn how our sales tax professionals can give you the peace of mind and confidence you’ll need during your audit.

Visit our resource pages for more information to help you make critical decisions during your New Mexico sales and use tax audit.

- The Audit Overview & Selection Process

- The General Audit Process

- Statute of Limitations Extensions & Issues

- Managing the Sales Tax Auditor

What to Expect from a New Mexico Sales Tax Auditor

If you want to know what to expect from a tax auditor, one way to do that is to study the playbook they are working from. You could read the New Mexico Auditors Manual if you find the time. For now, here is a summary of the general audit process:

- The auditor will conduct pre-audit research.

- The auditor will often schedule and perform an entrance conference.

- The auditor will request records (many of which the auditor is not entitled to and does not need)

Once the auditor receives the necessary records, they will compare your New Mexico sales and use tax returns to your federal income tax returns or bank statements to determine whether you reported all applicable or gross sales on your New Mexico sales tax return(s).

NOTE: A slight error in how the tax was charged on even a single type of transaction can add up to a significant sales tax liability.

Once the auditor is confident all sales are accounted for, they will:

- Review your exempt and out-of-state sales.

- Conduct a use tax audit – the auditor will request accounts documents to ensure you adequately paid use tax on applicable purchases.

Common areas audited include:

- Advertising Expense

- Auto & Truck Expense

- Repair and Maintenance

- Office Expense

- Miscellaneous Expense

- Supplies

- Equipment

If a business buys an item online without paying use tax, the business is still obligated to remit the tax to New Mexico. Believing otherwise often leads to shocking results for the unsuspecting taxpayer during an audit. Here is more information on New Mexico Use Tax.

If you have questions about your situation, contact us to discuss it with one of our tax professionals.

After the Audit – Understand and Defend Your Businesses Rights

Upon completion of the audit, there will usually be an exit conference with the auditor. The auditor will produce an audit report with corresponding work papers to support the New Mexico sales and use tax assessment.

It is advisable to have a sales tax professional present during this meeting. This is your first opportunity to see the auditor's findings. You'll want to push back on areas where they have overstepped their bounds or misapplied New Mexico's sales tax laws.

It's best to hold off on agreeing to the sales tax assessment until a sales tax professional has reviewed it for issues that should be challenged.

Many businesses wind up drastically overpaying the state because the business owner or in-house accounting personnel weren't well versed in the sales tax laws that, if challenged, could have reduced their sales tax liability. |

In the following sections, we'll cover the process of challenging a New Mexico sales tax audit assessment.

Contesting Audit Findings with the New Mexico Taxation and Revenue Department

New Mexico Sales Tax Audit Protest Process Flow Chart

Notice of Assessment Issued --> 90 days --> File Protest --> within 60 days --> Request informal conference --> within 180 days --> Hearing requested by either side with administrative hearings office --> 4-6 months --> Final Determination Issued --> 30 days --> Petition to New Mexico Court of Appeals.

NOTE: If the deadlines are missed, it can be tough to get the case reopened.

After an audit, the auditor will issue a Notice of Determination (AKA the audit report). It's essential to review and understand its implications carefully.

The audit report:

- Details of the auditor's findings

- Describes any proposed audit adjustments

- Shows the amount of tax, interest, and penalty due

If you disagree with the proposed changes, you may request an informal conference with the auditor. You must request an informal conference and attempt to resolve the case with the auditor.

Audit Closing Conference

The taxpayer has a short period to contest the findings with the auditor. Any issues with the results are handled as follows:

1. Issues related to exemptions, proof of tax paid, and calculations are worth addressing with the auditor.

2. Legal interpretations of sales tax law are often not resolvable at this stage.

After this conference, the auditor will adjust the audit assessment, and a Notice of Determination will be issued.

If you cannot resolve this with the auditor, the next step is to appeal/protest the issue.

Appeal/Protest with The New Mexico Taxation and Revenue Department

Should you disagree with the assessment, you may file a written protest with the Department within 90 days or pay the tax and submit a claim for a refund within the statute of limitations.

If you file a protest with the Department, you must pay the amount of tax, penalty, or interest not being protested. You do not need to pay the disputed tax, penalty, or interest until your protest is resolved.

Protests submitted more than 90 days after the assessment was mailed will not be considered; the amount assessed will become final, and NMDOR can pursue collections.

Protest Rights and Audit Finding Confirmation

If you received a Notice of Assessment and haven't talked to someone experienced in New Mexico State tax, now is the time. Do it before these deadlines are missed.

Administrative Hearing with The New Mexico Taxation and Revenue Department

The Protest Office reviews the protest filed and, if they disagree with your position, schedules a formal hearing within 180 days but no earlier than 60 days of filing a protest.

Within 60 days, you may request an informal conference. The Department must conduct an informal conference within 30 days after receiving your written request.

Final Decision

If the hearing officer's Decision and Order are to your satisfaction, your protest is resolved, and no further action is required on your part.

If you are not satisfied with the outcome of the administrative hearing, within 30 days of the decision, you can file an appeal to the Court of Appeals.

Our team has handled hundreds of administrative court cases. It can help your company receive the resolution you are entitled to. Get in touch with us today.

Settling a New Mexico Sales Tax Liability

After any critical notices are issued, settling your New Mexico sales tax case with the New Mexico Taxation and Revenue Department is possible by filing a New Mexico Offer in Compromise. The business must meet specific criteria to qualify, but you can get better results negotiating here than with the auditor.

However, knowing a fair settlement from an unreasonable settlement will be challenging without experience and knowledge of New Mexico's tax laws.

DO NOT attempt to negotiate a settlement without an experienced New Mexico state and local tax lawyer or other professional.

Contest a New Mexico Jeopardy Assessment

New Mexico may issue a Notice of Jeopardy Determination in certain situations.

The jeopardy assessment gives the New Mexico Taxation and Revenue Department the right to try to collect immediately.

Due to the jeopardy nature, the taxpayer only has a very short time to contest the assessment and must place a security deposit to fight the issue.

New Mexico Administrative Hearings Office

During the appeals process, either party can request an administrative hearing with the New Mexico Administrative Hearings Office. Frankly, there are few cases in which an administrative hearing should not be requested as a taxpayer. For the first time during your New Mexico tax audit, someone other than the New Mexico Taxation and Revenue Department hears your case. This independent state agency is designed as a neutral party to hear tax disputes against the state.

The administrative hearings also increase your chance of reaching a favorable settlement with the Taxation and Revenue Department. Like most states, as the case goes to the next level, each party, including the state, stands more to lose, and many cases are resolved at this level. If you have not at least contacted a state tax attorney or other professional, now is the time to do so.

Despite being a mere administrative hearing, the proceeding operates like a proceeding in a regular judicial court. The case begins with a petition and proceeds to a hearing. During the hearing, the taxpayer and the state can call witnesses for testimonial and documentation evidence. At the end of the case, the Administrative Law Judge issues a decision, which you can then appeal to the judicial court. This is another reason to have an experienced New Mexico tax lawyer, accountant, or other professional as part of your team.

As mentioned above, like many other areas of the law, most cases settle, and you should likely request an administrative hearing on your or your client’s case.

Other New Mexico Sales Tax Resources

New Mexico Taxation and Revenue Department Sales Tax Website

TP RIGHTS & PROTEST PROCEDURES [FYI] (newmexico.gov)

Recent Regulation Changes: All NM Taxes (newmexico.gov)

NMAC – State Records Center & Archives

If you received a Notice of Assessment and haven't talked to someone experienced in New Mexico State tax, now is the time. Do it before these deadlines are missed.

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.