California Sales and Use Tax & Audit Guide

This guide provides businesses with answers and explanations on the following California Sales and Use Tax topics:

- Do I need to collect California sales tax?

- Do I need to pay California use tax?

- What happens when I have an obligation to collect but didn’t?

- What steps can I take after receiving an audit notice?

- How to fight an improper sales tax assessment in California.

Who Needs to Collect California Sales and Use Tax?

California imposes a sales and use tax (SUT) on the purchase of certain tangible personal property and services within the state. If your business or your customers are located or have operations in California, SUT likely applies.

Nexus – How Is It Established in California?

According to the California Department of Tax and Fee Administration (CDTFA), nexus for paying sales tax in California occurs when a business has a physical presence in California. Some examples of physical presence could include:

- You have agents, including employees or contractors, who facilitate the sale of tangible personal property in California.

- You have an office or other place of business in California.

- You provide services related to personal property in California.

- Your business owns or leases property in the state.

- You deliver property into California for final use by a customer.

- You store inventory in California.

NOTE: California has been extremely aggressive in pursuing online retailers that use FBA services. California requires the fulfillment center to divulge sellers that use its fulfillment services and have inventory in California. If you use FBA or another fulfillment service, you are likely on California’s sales tax radar.

Additionally, businesses that do not have a physical presence in California can establish economic nexus by exceeding a certain annual sales threshold in the state. See the next section for details.

Economic Nexus (Wayfair Law) And Internet Sales in California

As of April 1, 2019, businesses located outside of California may still have sales tax obligations to the state. Specifically, California’s Wayfair law requires that a business register with CDTFA to collect and remit sales and use tax, regardless of physical location, if the business has sales in California exceeding $500,000 during the preceding or current calendar year.

Note: California counts all sales of tangible personal property toward the $500,000 threshold. This includes nontaxable sales, such as sales for resale.

Examples of Common Sales Subject to California Sales Tax

General Transactions

As a rule, California sales and use tax likely applies to your sales of personal property unless a specific exemption exists or California laws explicitly exclude your transaction from taxation. When questions arise for your business, schedule a time to review the taxability of your transactions with one of our sales tax professionals.

Common exemptions from California sales and use tax:

- Groceries, including candy, confectionery, and snack foods

- Medical devices

- Prescription medicines

- Housing-related utilities, such as gas, electric, water and steam

- Many entertainment industry-related purchases

- Many items used in farming or manufacturing.

Services

Generally, services are not subject to sales tax in California except for services that are “inseparable from the sale” of the tangible personal property. That said, there are a few services that are specifically subject to sales tax, such as digital or physical photographs and their related services.

Software

California does not tax software or software as a service (SaaS) unless the software is delivered on a tangible medium like a flash drive or CD.

Shipping & Handling

California maintains the following position on sales tax related to shipping and handling charges:

Shipping of non-taxable items:

- If the item being delivered is not taxable, the delivery charge is also non-taxable (that’s the easy part).

Shipping of taxable items:

- For taxable items, sales tax on the delivery charges depends on two things, how you invoice the charge and the actual cost of delivery compared to what you charge.

- Sales tax won’t generally apply when you separately state the shipping/delivery, freight, or postage on the invoice AND the charge is not greater than the actual delivery cost.

- If, however, the delivery charge is greater than the business’s actual cost, the portion of the charge that exceeds the actual delivery cost is taxable.

- Delivery charges can become fully taxable if:

- Adequate records of delivery costs are not kept,

- The delivery is made with your business’s own vehicles,

- You make a separate fuel surcharge or “handling” charge,

- Delivery is part of the price for the item sold, or

- “Freight-in” is included in cost.

Specific Industries

While the general sales tax rules seem straightforward, they can become difficult to apply in the context of certain industries. The CDTFA developed some industry-specific guidance on the application of California sales and use tax for items that may apply to your business.

- California Sales and Use Tax Guide for the Agricultural Industry

- California Sales and Use Tax Guide for Auto Repair Garages and Service Stations

- California Sales and Use Tax Guide for Gas Station Operators

- California Sales and Use Tax Guide for Barbers and Beauty Shops

- California Sales and Use Tax Guide for Wineries and Wine Distributors

- California Sales and Use Tax Guide for Liquor Stores

- California Sales and Use Tax Guide for Beer Breweries and Distributors

- California Sales and Use Tax Guide for Distilleries and Liquor Distributors

- California Sales and Use Tax Guide for the Dining and Beverage Industry

- California Sales and Use Tax Guide for Restaurants, Bars, Caterers and Hotels

- California Sales and Use Tax Guide for the Cannabis Industry

- California Sales and Use Tax Guide for Construction and Building Contractors

- California Sales and Use Tax Guide for Dry Cleaners

- California Sales and Use Tax Guide for Elective Ultrasound Services

- California Sales and Use Tax Guide for Fulfillment Centers

- California Sales and Use Tax Guide for the Gig Economy

- California Sales and Use Tax Guide for Green Technology

- California Sales and Use Tax Guide for Grocery Stores

- California Sales and Use Tax Guide for Gun Dealers

- California Sales and Use Tax Guide for Mobile Phone Vendors

- California Sales and Use Tax Guide for Car Dealers and Dealerships

- California Sales and Use Tax Guide for Photography

- California Sales and Use Tax Guide for Purchase of Log Homes

- California Sales and Use Tax Guide for Venue Rental Businesses

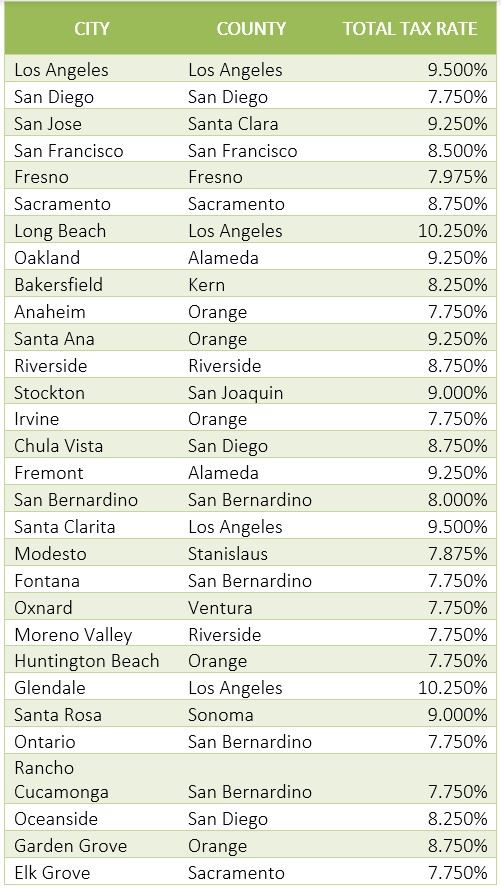

Determining Local Sales and Use Tax Rates in California

California has a base sales tax rate of 7.25%. This is the minimum rate that applies to your taxable sales unless a rate deduction exists. However, your sales may have a rate higher than 7.25% if city or county surtaxes apply. Local rates in California can range from 0.10% to 1.00%, and some areas may have more than one surtax rate in effect.

The district surtax applies if the sale occurs or you deliver property to a location within the respective county. State and local taxes are remitted to the state as part of the California sales and use tax return. The combined California + local sales and use tax rates for the largest 30 cities as of January 1, 2023, are listed below. A comprehensive list can be found here.

I Should Have Collected California Sales Tax, But I Didn’t

If you determine your business has nexus in California, but you have not collected or remitted California sales tax, primary options include:

- Registering for a seller’s permit with the CDTFA and paying your tax liability (which could include penalties and interest), or

- Entering a Voluntary Disclosure Agreement (VDA) to potentially eliminate penalties and reduce tax liability.

When deciding which options may be best for your business’s situation, consider the following:

Option 1: Register to Pay Back Taxes, Penalties, and Interest

Sometimes the best solution for a business is simply to register with California and pay back taxes, penalties, and interest. A VDA is not always cost-effective depending on the amount of your liability. If you’re unsure of that amount, contact us for an analysis of the potential scope of your liability.

When to consider registration and payment:

- Your nexus with California is less than 3 years old.

- The sales tax penalty is LESS than the cost of a VDA.

- Your business did not collect (but fail to remit) California sales tax.

Note: Registering with the CDTFA does not waive past sales tax liability you might have.

Option 2: Voluntary Disclosure Agreement (VDA)

California’s VDA program limits the scope of your sales tax liability to the past 3 years. Voluntary disclosures are a useful tool to reduce extended periods of sales tax exposure. In other words, when you have nexus with California that began longer than 3 years ago. As a result, the benefit of a VDA usually depends on:

- How long you’ve had nexus with California but failed to file or pay taxes.

- Your potential sales tax penalty savings is MORE than the cost of a professional to help you get a VDA.

- You have a sales tax collected but not remitted issue.

I Received a California Sales and Use Tax Audit Notice, What Should I Do?

California regularly audits businesses to review their sales tax compliance and recover uncollected amounts. Businesses might consider professional help with their CDTFA audit based on the following issues:

- Your lack of experience with sales tax audits and your ability to contest unfair practices from the auditor that violate procedure.

- Your ability to manage the transfer of sensitive business documents.

- You lack clarity on your overall sales tax exposure.

Controlling the audit from the start could be helpful in limiting exposure. Are you confident in doing that on your own? Contact us and learn how our sales tax professionals can give you the peace of mind and confidence you need during a CDTFA audit.

Additionally, these resource pages are full of detailed information to help you evaluate critical decisions during your California sales and use tax audit.

- The Audit Overview & Selection Process

- The General Audit Process

- Statute of Limitations Extensions & Issues

- Managing the Sales Tax Auditor

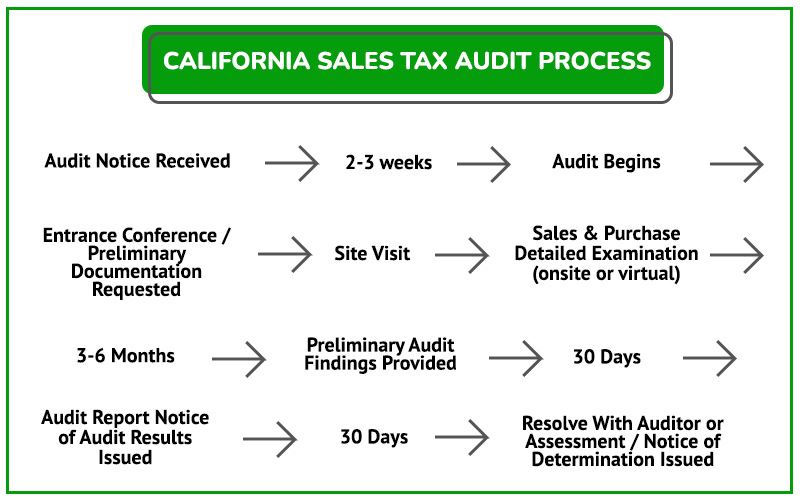

California Sales Tax Audit Process

See the detailed guidance for each stage of the audit process in the flowchart below.

What to Expect After You Receive a California Sales and Use Tax Audit Notice

Most audits start with notice from the CDTFA made in writing and via a phone call from a sales tax auditor. The moment after you receive an audit notice is when we highly recommend you consider hiring a state and local tax professional to prepare.

What to Expect From A California Sales Tax Auditor

- Auditor will review available information like SUT returns.

- You will have an entrance conference with the auditor.

- The auditor may request certain business records like bank statements or receipts.

What to Expect During The Audit

Once the necessary records are received, the auditor will:

- Conduct the sales tax audit by analyzing available records to determine if you have any unreported sales or if your reported sales are below industry expectations.

- Once the auditor is confident all sales are accounted for, they will review your exempt and out-of-state sales.

After the Audit – Understand and Defend Your Businesses Rights

After review, the auditor will prepare an audit report and hold an exit conference to share the findings with you. This will be the first time when you learn about the potential for outstanding sales tax liability, including accrual of any interest or penalty. Again, having a sales tax professional is helpful in this stage to potentially challenge findings or the auditor’s process on the spot.

The exit conference is also when the auditor may request your signature on a form where you agree to the audit findings. We recommend businesses refrain from agreeing to the sales tax assessment until after a sales tax professional has reviewed it for errors and potential challenges. Many businesses fail to appreciate the flaws in an audit that can arise because of misunderstanding or human error.

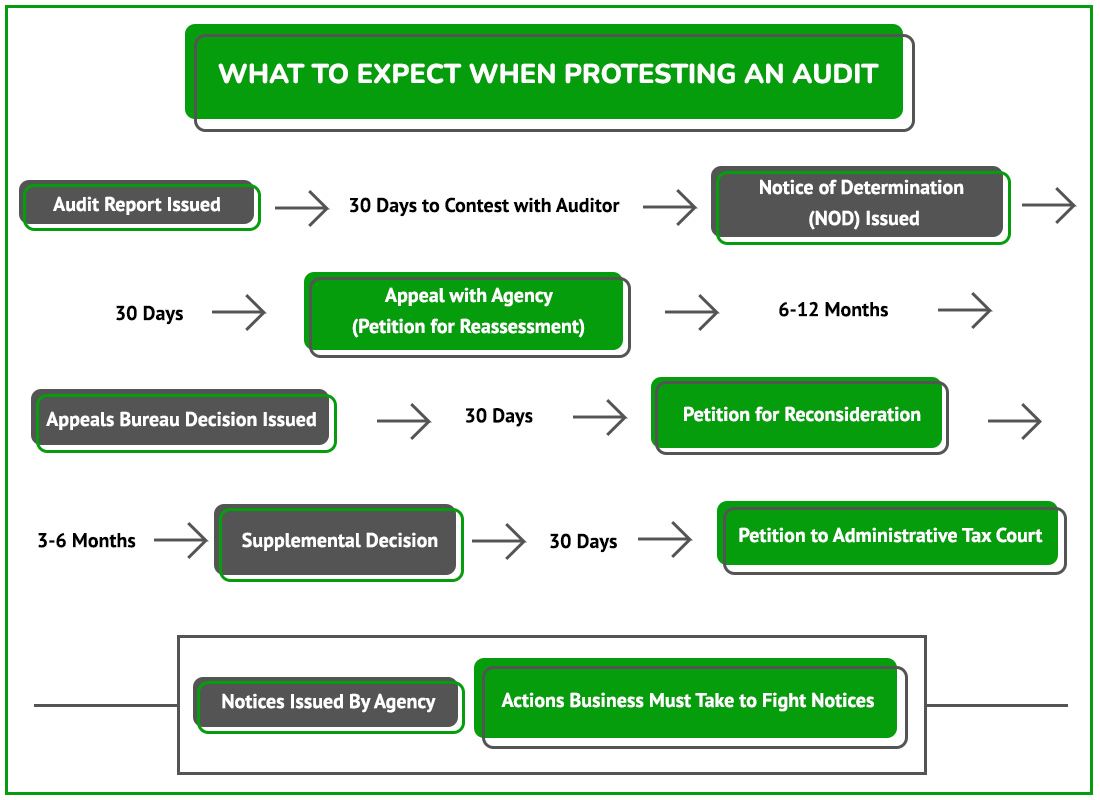

The following process of protesting a California sales tax audit assessment may be useful depending on your case.

NOTE: If a NOD deadline is missed, you have an additional 30 days to file in administrative court. Reopening your audit after missing that deadline can be difficult, if not impossible.

Contesting Audit Findings with the Auditor

After an audit, the auditor will issue a California Notice of Audit Results (AKA the audit report). This document details the auditor’s findings so it’s important to carefully review and understand its implications. Any issues with the results are handled as follows:

- You generally have 30 days to contest findings with the auditor, which might involve documentational issues like:

- Use of exemption certificates

- Proof that tax was paid

- Sales tax calculations

- Sampling methods or other field audit concerns

- Legal interpretations of sales tax law are often not resolvable at this stage.

- If a resolution cannot be reached with the auditor, the next step is to appeal the issue with the CDTFA.

Appeal / Protest with the California Department of Tax and Fee Administration

Appeal to the CDTFA is done after you receive the Notice of Determination and you should keep the following in mind:

- A Petition for Redetermination must be done within 30 days of the Notice of Determination (NOD) issuance.

- If you miss the 30 days, you may have an additional 30 days to file in administrative or judicial court to challenge the audit findings.

- If both periods are missed, the audit and accompanying assessment become final.

If you received a Notice of Determination and have not talked to someone experienced in California State and Local tax, now is the time to avoid the risk of missing an available protest deadline.

Appeals Bureau Decision

If you cannot resolve the California sales and use tax dispute through the protest process, the California Department of Tax and Fee Administration will issue an Appeals Bureau Decision. The Appeals Bureau Decision gives you the opportunity to re-protest the assessment within the administration or file in California’s administrative tax court, which is called the California Office of Tax Appeals. There are important deadlines for this appeal option too, such as 30 days to re-protest or 30 days to file in administrative court.

Settling a California Sales Tax Liability

Along the way, you may have a chance to settle your California sales tax case by negotiating with CDTFA. Often, you can get better results here than with the auditor because they have limited authority. If you or your CPA or bookkeeper seldom does state and local tax work, it might be difficult to evaluate fair versus unreasonable settlements. DO NOT try to negotiate a settlement without an experienced California state and local tax lawyer or other professional.

Contest a California Jeopardy Assessment

California may issue a Notice of Jeopardy Determination in certain situations. The jeopardy assessment gives CDTFA accelerated rights for collecting unpaid tax. Due to the jeopardy nature, the taxpayer only has a short period of time to contest the assessment and must place a security deposit to fight the issue without further action being taken against them.

California Administrative Court

If you cannot get your audit resolved within the agency or your deadlines have been missed, you still have one last shot to fight your California sales tax assessment by going to California Office of Tax Appeals. In some cases, it may make sense to skip the protest to the CDTFA and file directly in administrative court.

If your case is filed in administrative court, and the case proceeds to hearing, it is heard and decided by a neutral panel of administrative law judges. Our team has handled hundreds of administrative court cases involving sales and use tax and can help your company achieve a resolution. It is very similar to a court hearing and having an experienced representative could be useful.

Other California Sales Tax Resources

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.