Arkansas Sales and Use Tax & Audit Guide

This guide is for businesses that need straightforward answers on the following Arkansas Sales and Use Tax subjects:

- Should I collect Arkansas sales tax?

- What is Arkansas use tax, and should I pay or collect it?

- I collected Arkansas sales tax and did not remit it, now what?

- I received a Notice that I’m being audited by the Arkansas Department of Treasury, now what?

- Guidance on fighting a sales tax assessment in Arkansas.

Who Needs to Collect Arkansas Sales and Use Tax?

Businesses that have nexus with Arkansas and make taxable sales or purchases will likely need to register for a permit with the Arkansas Department of Finance and Administration to report and pay tax also referred to as a gross receipts tax.

How Is Nexus Established in Arkansas?

According to the Arkansas Department of Treasury, sales tax nexus could occur if a business has a physical presence in Arkansas. Some examples of qualifying conduct could include:

- Maintaining an office or space in Arkansas to conduct business.

- Having independent sales reps, employees, or agents conducting business, permanently or temporarily, in the state, including soliciting sales, collecting on current or delinquent accounts delivering property, or taking orders for taxable items in Arkansas.

- Performing services, such as assembling, installing, servicing, or repairing products in Arkansas.

- Providing services, such as maintenance or repairs to property.

- Providing customers technical assistance or services including, but not limited to, engineering assistance, design service, quality control, product inspections, or similar services.

- Owning, renting, or leasing real property or tangible personal property in Arkansas, including a computer server or software to solicit orders for taxable items.

- Using your company-owned or leased truck to deliver goods to customers within Arkansas.

- Maintaining inventory in Arkansas using a third-party fulfillment service, such as Fulfilled by Amazon (“FBA”).

Additionally, business that do not have a physical presence in Arkansas (i.e., remote sellers) could still have nexus by exceeding a certain annual sales threshold in the state, which is commonly referred to as economic nexus. More on that below.

Economic Nexus (Wayfair Law) and Internet Sales in Arkansas

Starting July 1, 2019, Arkansas required that remote sellers register with the Arkansas Department of Finance and Administration to collect and remit sales and use tax. If the business has either in the current or preceding twelve calendar months: (1) a total sales revenue in the state of more than $100,000 or (2) has more than 200 transactions, then it needs to register for tax.

See Arkansas Remote Seller FAQs for more information.

Arkansas Sales Made Through Marketplace Facilitator

If your business sells on Amazon or a similar service, you may or may not have to collect sales and use tax on those sales depending on your contractual agreement, if any, with that marketplace facilitator. Specifically, this may be the case if the marketplace facilitator certifies they are collecting and reporting sales tax on your behalf. However, such sales may count towards your total sales threshold, potentially requiring your business to collect tax on sales made directly through your website or another marketplace facilitator.

Which Sales Are Subject to Arkansas Sales Tax?

General Transactions

Most sales of goods and services in Arkansas will trigger sales and use tax obligations of some kind. If you have nexus in Arkansas, your business has the burden of knowing whether the products or services it sells are subject to Arkansas sales and use tax. Like other jurisdictions, unless an item is specifically exempt, sales and rentals of tangible personal property are subject to Arkansas sales tax.

We recommend scheduling a time to review your specific situation with one of our sales tax professionals if you are unsure of the taxability of an item in Arkansas.

Common exemptions from Arkansas sales and use tax:

- Machinery and Equipment

- Farm Equipment

- Livestock Feed

- Products for Agriculture Production

- Prescription Drugs

- Certain Packaging Materials

Services

Generally, services are not subject to Arkansas sales tax unless specifically included under Arkansas Code. The following services listed here are subject to Arkansas sales tax as a result:

- Wrecker and Towing Services

- Solid Waste Disposal and Collection Services

- Parking Lot and Gutter Cleaning Services

- Pest Control

- Both Commercial and Personal Laundry and Dry Cleaning

- Body Piercing, Tattoo, and Electrolysis Services

- Security and Alarm Monitoring Services

- Locksmith Services

- Boat Storage and Docking Fees

- Certain Furnishing of Camping or Trailer Space Rentals

- Pet Grooming and Kennel Services

Software

Arkansas broadly treats the sale of computer software and prewritten computer software as the sale of tangible personal property subject to gross receipts tax, except when delivered electronically or by load and leave. Software maintenance contracts are not generally subject to tax. For questions on the taxability of Software as a Service (SaaS) in Arkansas, schedule a consultation with our consultants.

Shipping & Handling

Arkansas includes all freight, shipping, and transportation charges as part of the gross receipts subject to sales tax, regardless of being separately stated on the invoice, when billed through the retailer. However, freight charges billed directly to the buyer through a carrier service are generally exempt.

Specific Industries

While the general sales tax rules seem straightforward, the application can be difficult in gray areas that exist because of new industries and undeveloped sales tax regulations. The Arkansas Department of Finance and Administration offers additional guidance to businesses with specific sales tax issues through its Gross Receipts Tax Rules . While these rules may provide some help, they may not be responsive to all your Arkansas sales tax questions. Consider scheduling a consultation with our sales tax professionals with specific questions about the taxability of your sales or purchases.

Determining Local Sales and Use Tax Rates in Arkansas

Arkansas’s base or statewide sales tax rate is 6.500%. In addition to the base rate for Arkansas state sales tax, your business may be subject to city and county rates that could apply depending on where your business is located or where you deliver products to customers.

Sales & Use Tax Rates in Arkansas

The combined state and local Arkansas sales and use tax rates for the largest counties are listed below, but you may also need to consider applicable city rates which can be found here.

I Should Have Collected Arkansas Sales Tax, But I Didn’t

If you have nexus with Arkansas, but have not been collecting tax, then you have an increased risk of future audit and assessment. Remote sellers who find themselves in this position usually have a couple of options for getting compliant with the Arkansas Department Finance and Administration (DFA):

- Register and pay back taxes, penalties, and interest, or

- Participate in the Arkansas Voluntary Disclosure Program.

Here is what you need to know about each option to make the best decision for your business:

Option 1: Register to Pay Back Taxes, Penalties, and Interest

Sometimes the best solution for a business is simply to register with Arkansas and pay back taxes, penalties, and interest. This is often the case when your past liabilities (including penalties) are low. Be cautious of the tax professionals that recommend doing a VDA in all situations, they are looking to make a buck rather than looking out for your best interests.

If you’re unsure what your past liabilities are, contact us and one of our state tax professionals will work with you to conduct an analysis and help you make the right choice for your business.

When to consider registration and payment:

- If you established nexus less than 3 years ago.

- The sales tax penalty is LESS than the professional fees charged for the VDA.

- Your business does NOT have a sales tax collected issue.

Beware: registering does not remove your past liabilities, so it’s critical to know the amount of sales tax exposure you have beforehand.

Option 2: Voluntary Disclosure Agreement (VDA)

Arkansas’s lookback period: 3 years.

In many situations, voluntary disclosures are a useful tool to reduce extended periods of past exposure. For example, if you should have been collecting sales tax for 10 years, the voluntary disclosure limits the lookback period to 4 years. As a result, the benefit of doing a VDA often turns on:

- Whether the VDA limits lookback period. i.e. – you established nexus more than 4 years ago.

- The sales tax penalty savings are MORE than the professional fees charged for the VDA.

- You have a sales tax collected but not remitted issue.

I Received an Arkansas Sales and Use Tax Audit Notice, What Should I Do?

The Arkansas DFA regularly audits businesses that are required to charge, collect, and remit various taxes in the state. Businesses that receive sales and use tax audit notice should consider their overall ability to manage an Arkansas sales tax audit on their own, including the handling of issues like:

- Familiarity with Arkansas’s sales and use tax laws to know the audit process is being done correctly.

- The disclosure of your sensitive business information in response to record requests from the auditor.

- Knowing your sales and use tax exposure in Arkansas to confidently weight settlement offers and appeal options.

- Limiting your sales tax exposure through controlling the audit process.

When you have doubts about your experience or ability to handle an Arkansas sales tax audit, hiring a professional might be right for you. Contact us and learn how our sales tax professionals can give you the peace-of-mind and confidence you need during your audit.

Please visit our resource pages for more detailed information and to help you evaluate critical decisions during your Arkansas sales and use tax audit.

- The Audit Overview & Selection Process

- The General Audit Process

- Statute of Limitations Extensions & Issues

- Managing the Sales Tax Auditor

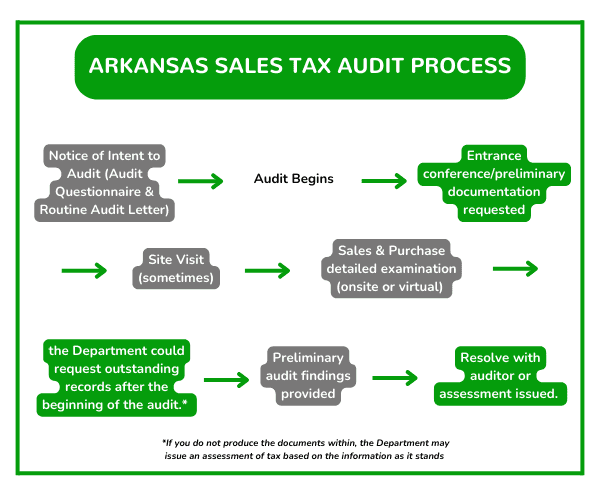

Arkansas Sales Tax Audit Process

The audit process usually follows the process laid out in this flowchart. See the detailed guidance for each stage of the process in the sections below.

What to Expect After You Receive an Arkansas Sales and Use Tax Audit Notice

Many audits begin with a random call from the Arkansas DFA sales tax field auditor. Shortly after, your business will receive an audit notice which confirms that your business was chosen for an Arkansas sales and use tax audit. To prepare for the audit, it is likely a good idea to start by getting a state and local tax professional involved.

What to Expect from an Arkansas Sales Tax Auditor

- Auditor will conduct pre-audit research of your business.

- Auditor will often schedule and perform an entrance conference.

- Records will be requested (many of which the auditor is not entitled to and does not need).

- Auditor will determine the type of audit necessary based on the available records (i.e., a detail audit or a sample audit).

What to Expect During the Audit

Once the necessary records are received, the auditor will:

- Conduct the audit by comparing your Arkansas sales and use tax returns to your federal income tax returns or bank statements to determine whether all applicable sales, or gross sales, were reported on your Arkansas sales tax return(s).

NOTE: A slight error in how tax was charged on even a single type of transaction, when multiplied over several years, can add up to a considerable sales tax liability.

- Once the auditor is confident all sales are accounted for, they will review your exempt and out-of-state sales.

- The auditor will next conduct a use tax audit where they will request a detail of certain documents and accounts to make sure use tax was properly paid on business expenses. Common areas audited for payment of use tax include:

- Advertising Expense

- Auto & Truck Expense

- Repair and Maintenance

- Rent (including related party rent)

- Office Expense

- Miscellaneous Expense

- Supplies

- Equipment

Note on online purchases of business expenses. Despite publications to the contrary, if a business buys an item online without paying use tax, the business still has an obligation to remit the use tax to Arkansas when consumed or stored in the state. This often leads to shocking results for the unsuspecting taxpayer during an audit.

After the Audit – Understand and Defend Your Businesses Rights

Upon completion of the audit, there will usually be an exit conference with the auditor. The auditor will produce an audit report with audit schedules to support the proposed adjustment of your Arkansas sales and use tax assessment. It is advisable to have a sales tax professional present during this meeting as this is your first opportunity to see the auditor’s results and dispute any of the findings.

The Arkansas DFA will then issue a Notice of Assessment, which will state the tax, penalty, and interest owed. Once received, you have two options. You can either pay the amount stated on the assessment or pursue further appeal options with the DFA or Arkansas state court.

We recommend businesses refrain from agreeing to the sales tax assessment until after a sales tax professional has reviewed it for potential issues to challenge. This way, you can make an informed choice about your tax assessment before making payment. Many businesses wind up drastically overpaying the state of Arkansas because the business owner or in-house accounting personnel were not well versed in the sales tax laws that, if challenged, could have reduced their Arkansas sales tax liability.

See the Arkansas Taxpayer’s Bill of Rights for more information.

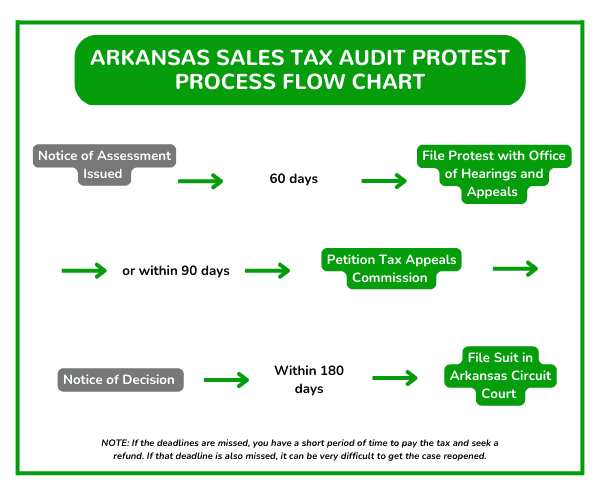

Below, we explain the process of further challenging an Arkansas sales tax audit assessment.

Arkansas Sales Tax Audit Protest Process Flow Chart

NOTE:If the deadlines are missed, you have a short period of time to pay the tax and seek a refund. If that deadline is also missed, it can be very difficult to get the case reopened.

Contesting Audit Findings with the Auditor

After an audit, the auditor will issue an Arkansas Notice of Audit Results (AKA the audit report). This document details the auditor’s findings so it’s important to carefully review and understand its implications. Any issues with the results are handled as follows:

- Auditee has from the date stated on the notice to contest findings with the auditor.

- Documentational issues (e.g., exemption certificates, proof tax was paid, etc.) and calculations are worth addressing with the auditor at this stage.

- Legal interpretations of sales tax law are often not resolvable at this stage and require further appeal.

- If a resolution cannot be reached with the auditor, the next step is to request a reconsideration of the audit issue with the Arkansas DFA.

Appeal with the Arkansas DFA’s Office of Hearings and Appeals

You can further appeal any contested issues that were unresolved before receipt of the Final Assessment Notice through the Arkansas DFA’s Office of Hearings and Appeals. This is a separate office from the DFA’s Field Audit Office that includes administrative law judges who will hear your sales tax dispute and render a written opinion. Keep the following in mind when it comes to requesting an appeal:

- A protest of your assessment must be done within 60 days of the DFA issuing the proposed assessment notice.

- If you miss the 60 days, you could have additional time to pay the tax and file a refund claim in some cases.

- If both periods are missed, the assessment usually becomes final, and it is very difficult to reopen the audit.

- You have a right to representation from an attorney, CPA, or sales tax professional during the appeal and hearing process.

- If you disagree with the administrative judge’s opinion, you may request the Secretary of the Arkansas DFA to revise the decision of the hearing officer.

If you have received a Notification of Audit Results or a Proposed Assessment and have not at least talked to someone experienced in Arkansas State and Local tax, now is the time before your initial appeal deadline lapses.

Judicial Appeal of Final Assessment to the Arkansas Tax Tribunal or Court of Claims

If you cannot resolve the Arkansas sales and use tax dispute through the appeal process, the Arkansas DFA will issue a Final Assessment. The Final Assessment gives you the opportunity to file a judicial appeal in the Arkansas Circuit Court with jurisdiction taking place in either Pulaski County Circuit Court or the circuit court of the county where your business is located.

There are important deadlines in this phase of the process as well, such as having 180 days to file a suit from the date of final assessment or decision from the DFA. Alternatively, you could pay the entire amount of Arkansas state sales tax due within one year of assessment and have one year to file suit from the date of payment. Further appeal can then take place with the Arkansas Supreme Court.

Settling a Arkansas Sales Tax Liability

In certain situations, you may have an opportunity to negotiate and settle your sales tax liability through an Offer in Compromise with the Arkansas Department of Treasury. Often, you can get better results here than with the auditor. If you or your professional seldom does state and local tax work, it might be difficult to evaluate fair versus unreasonable settlements. DO NOT try to negotiate a settlement without an experienced Arkansas state and local tax lawyer or other professional.

Contest an Arkansas Jeopardy Assessment

Arkansas may issue a Notice of Jeopardy Assessment in certain situations. The jeopardy assessment gives the Arkansas DFA accelerated rights and it may immediately begin to try and collect. Due to the jeopardy nature, the taxpayer only has 5 days to file a protest of the assessment.

Other Arkansas Sales Tax Resources

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.