Maryland Sales Tax & Audit Guide

Straightforward Answers to Your Maryland Sales Tax Questions.

- Do I need to collect Maryland sales tax?

- Should I be collecting or paying Maryland use tax?

- What do I do if I should have been collecting but haven't?

- I received an audit notice. What should I do?

- Guidance on fighting a sales tax assessment in Maryland.

Who Needs to Collect Maryland Sales and Use Tax?

Like most states, to be subject to Maryland sales tax collection and its rules, your business must:

1) Have nexus with Maryland, and

2) Sell or use something subject to Maryland sales tax.

How is Nexus Established in Maryland?

According to the Comptroller’s Office of Maryland, anyone who sells taxable tangible personal property, recreational activities admissions, or the rental of lodging accommodations must obtain a sales tax permit.

Any of the following establishes nexus:

- Maintains or uses any office, storage, warehouse, or another place of business in the State.

- Has an agent, or other representatives, salesperson, or solicitor working in the State to deliver, sell, or accept orders for tangible personal property or taxable service.

- Entering the State regularly to provide repair or other services for tangible personal property.

- Regularly uses vehicles to sell or deliver tangible personal property or a taxable service for use in the State; or

Additionally, businesses that do not have a physical presence in Maryland can establish economic nexus by exceeding a certain annual sales threshold.

Economic Nexus (Wayfair Law) and Internet Sales in Maryland

A remote seller or a marketplace facilitator who sells tangible personal property or taxable services for delivery in the State must register to collect Maryland sales and use tax if, in the previous or current calendar year, the seller satisfies at least one of the following criteria:

- Gross revenue from the sales of tangible personal property or taxable services delivered in the State exceeds $100,000; or

- Sold tangible personal property or taxable services for delivery into the State in 200 or more separate transactions.

How are the $100,000 gross revenue and the 200 transaction thresholds calculated?

Gross sales are calculated as the total sales revenue from direct sales. Do not include any facilitated sales or tax collected in this figure.

Marketplace Sellers

A marketplace seller offers tangible personal property or other products or services subject to Maryland sales or use tax through a marketplace owned, operated, or controlled by a marketplace facilitator. Suppose your business sells through Amazon or a similar marketplace facilitator. In this case, you may not have to collect sales tax on those sales.

Specifically, if the marketplace facilitator certifies that they collect and report sales tax on your sales, you are off the hook. However, such sales may still count towards your total sales threshold, meaning you’ll still need to collect tax on sales made directly through your website or any other marketplaces that do not collect sales tax on your behalf.

Which Sales are Subject to Maryland Sales Tax?

General Transactions

Taxes in Maryland are on transactions and not on items. Five kinds of transactions are subject to the tax:

▪ Sale of property in Maryland.

▪ Leasing or licensing property employed in Maryland.

▪ Granting a right to use a franchise in Maryland.

▪ Performance of services* in Maryland

The law presumes that all transactions are taxable unless a statute provides an exemption or deduction. See FYI-105, "Gross Receipts and Compensating Taxes: An Overview" for a listing of exemptions and deductions.

We recommend scheduling a time to review your specific situation with one of our sales tax professionals.

Common Exemptions from Maryland Sales and Use Tax:

Exempt items include:

- Baby Products

- Oral Hygiene Products

- Food

- Medical Devices and Products

- Medicine and Medical Equipment

- Newspapers

- Food for Human Consumption

- Construction Materials

- The material is purchased to further the construction or redevelopment of a sports entertainment facility or a Prince George's County Blue Line Corridor facility.

- The sale is made on or after October 1, 2021, and

- the buyer provides the retailer with evidence of eligibility for the exemption

- Repairs of Tangible Personal Property

- Restoring tangible personal property to its original condition or usefulness is not taxable. The creation of a new item is a fabrication, which is taxable.

- If you repair personal property, you DO NOT have to pay tax on purchases of:

- Parts that you resell over the counter

- Parts installed on or in customer property under mandatory maintenance contracts; or

- Components that the seller will install on property you are repairing and for which a separate charge will be made.

- You DO have to pay the tax on:

- Purchases of parts and supplies included in lump-sum billing; and

- Items you use for the job, such as tools

- , do not become a part of the repaired property—for example, soaps, rags, masking tape, and sandpaper.

For additional information, view Business Tax Tip #7 and Business Tax Tip #8.

- Production Activities

- The following are tax-exempt production activities:

- Assembling, processing, manufacturing, or refining tangible personal property for sale or resale (except for processing food or beverages by a food vendor);

- Generating electricity for sale or use in production activities.

- Establishing/maintaining clean rooms/clean zones required by federal laws to manufacture drugs, medical devices, and biologics.

- Producing, maintaining, or repairing production machinery or equipment.

- Laundering, preparing, and maintaining textiles in providing the taxable service of commercial cleaning or laundering of materials for a buyer engaged in a business that regularly requires this service of commercial cleaning/laundering of the textiles.

- Providing safety glasses, hard hats, and breathing apparatus for the safety of employees.

- Providing quality control.

- The following are tax-exempt production activities:

- Tax-exempt items include:

- Any tangible personal property used directly and predominantly in a production activity in any stage of operation on the production activity site - from handling raw materials or components to moving finished products.

- Foundations to support other machinery, equipment, or items required to conform to air or water pollution laws and customarily considered part of real property.

- Safety equipment for use in a production activity.

- Quality control equipment and machinery that is used at a production activity site.

- Supplies and equipment used to remove finished goods on a production activity site.

- Machinery used to produce bituminous concrete and

- specific equipment used in aluminum production.

- Sales tax is not imposed on core charges made in connection with sales of these re-manufactured truck parts and their components:

- Air brake systems

- Engines

- Rear axle carriers

- Transmissions

- Sales of fuel and utilities are exempt from Maryland's sales and use tax under the same terms as other consumables.

- Agricultural

- Sales and rentals of farm equipment to a farmer for use in raising livestock and poultry, preparing, irrigating, or tending the soil or plant, or to service, harvest, store, clean, dry, or transport seeds or crops are exempt.

- Commercial aquaculture is treated the same as commercial agriculture.

- Exemptions are available for capitalized equipment and consumables purchases by farmers growing food.

The exemptions are explained in Business Tax Tip #9.

Services

Transactions for services are generally taxed where the service is provided to the customer.

- Janitorial Services

- Security Services

- Advertising Agencies

- Detective Services

- Photography

- Dry Cleaners and Laundries

- Florist

- Real Property Construction, Improvement, Alteration, and Repair

Software

Often, people have questions about the taxability of Software as a Service (SaaS).

Many states already impose a tax on Software as a service. As these options proliferate, states are moving to update their tax laws and, naturally, impose a tax.

To determine whether you need to collect tax on software sales, we highly recommend contacting one of our sales tax professionals to help you sort it out.

You can find more details about Maryland sales tax and Software as a Service here. Still, we have provided the basic information below to help you get started.

As of April 11, 2022, digital products do not include the following:

(1) a product having electrical, digital, wireless, magnetic, optical, electromagnetic, or similar capabilities when the purchaser holds a copyright or other intellectual property interest, in whole or in part, if the purchaser uses the product solely for commercial purposes, including advertising or other marketing activities; or

(2) computer software or software as a service (SaaS) that is purchased or licensed solely for commercial purposes in an enterprise computer system. This includes operating programs or application software for the exclusive use of the enterprise software system that is housed or maintained by the purchaser or on a cloud server, whether hosted by the purchaser, the software vendor, or a third party.

Shipping and Handling

Separately stated shipping charges are deductible, but the deduction is lost if it is

combined with handling charges and not stated separately on the invoice to the purchaser.

Industry-Specific Guidance

While the general sales tax rules seem straightforward, applying those rules can get tricky when gray areas arise. The Comptroller’s Office of Maryland provides some specific guidance for the following industries and special situations:

- Flea Markets

- Purchases for Resale

- Sales of Food

- Out-of-State Purchases

- Modular Buildings

- Transient Vendors

- Alcohol Sales Tax

- Bulk Sales Tax

- Mobile Homes

- Tax Included Sales

- Sales By Parent Teacher Organizations and Other Organizations

- Fabrication and Labor

- Bulk Vending Machine Sales

- Combined Sales

- Canceled and Returned Sales

- Sales Where It is Impractical to establish the Amount of Property to be Resold

- "Taxable price" Defined

- Sale of Medicines, Medical Supplies, and Sickroom Equipment

- Natural and Artificial Gas, Electricity, Steam, Oil, and Coal

- Printing

- Casual and Isolated Sales

- Certain Capital Transaction

- Resale Certificates

- Containers

- Games and Amusements

- Time of Collection

- Exempt Organizations

- Room Rentals

- Tangible Personal Property Consumed in a Production Activity

- Transactions in Interstate Commerce

- Aircraft, Motor Vehicles, Railroad Rolling Stock, and Vessels Used in Interstate and Foreign Commerce

- Auctioneers, Agents, Brokers, and Factors

- Lease of Tangible Personal Property

- Ice

- Fabrication or Production

- Direct Payment Permits

- Machinery and equipment for use in a Production Activity

- Tangible Personal Property Used in a Manufacturing & Process

- Tangible Personal Property Used in a Production & Activity

- Out-of-State Vendor

- Special Use tax on certain electricity

- Property or Services Used in Film Production Activity

- Signs

- Tax-free Week for Qualifying Clothing and Footwear Items

- Cellular Telephones and Other Mobile Telecommunications Services Charges

- Sales of Appliances Meeting Certain Efficiency Requirements and Multifuel Pellet Stoves

- Effective Rate Agreements

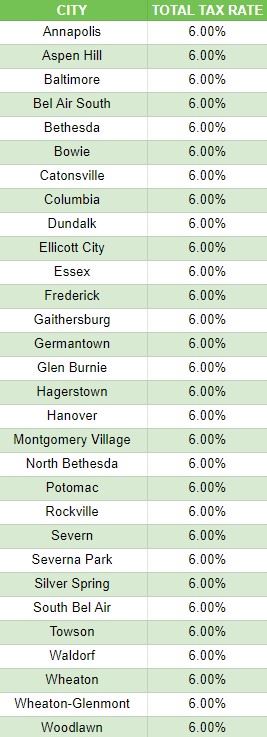

Determining Local Sales Tax Rates in Maryland

The Maryland state sales and use tax rate is 6%. Localities in Maryland impose no specific tax; however, the sales tax collected varies for the following:

- Alcoholic beverages are sold based on a 9% sales tax rate.

- An 11.5 percent tax is imposed on short-term car and recreational vehicle rentals.

- Some short-term truck rentals are subject to an 8 percent tax.

- A 6% tax rate applies to a portion of the sale of new mobile homes and modular buildings and a part of the gross receipts from vending machine sales.

Local Sales and Use Tax Tables

Here you can look up local Maryland sales tax rates. Or find your city’s local tax rate in the chart below:

*Exact tax rates vary. Occupancy fees and taxes are not included in this table.

I Should Have Collected Maryland Sales Tax, But I Didn't

Many of our competitors suggest filing a Voluntary Disclosure Agreement in each State. This is a one-size-fits-all solution that is not always the best. Our sales tax professionals will work with you to determine your business's best and most cost-effective solution.

If you determine your business has nexus, but you have not collected Maryland sales tax, here are your options:

1. Register and pay back taxes, penalties, and interest, or

2. Complete a VDA to cut penalties (and, in some cases, reduce your tax liability and avoid interest).

This is what you need to know about each option to make the best decision for your business:

Option 1: Register to Pay Back Taxes, Penalties, and Interest

A VDA is not cost-effective if the past liabilities and penalties are minimal. Sometimes the best resolution for a business is to register with Maryland and pay back taxes, penalties, and interest.

Be wary of the tax professionals recommending a VDA in these cases. They want to make a buck rather than look out for your best interests.

When to consider registration and payment:

- If you established nexus less than 3 or 4 years ago.

- The sales tax penalty is LESS than the professional fees charged for the VDA.

- Your business does NOT have a sales tax collected issue.

Beware: Registering does not generally end past liabilities.

If you are unsure what your past liabilities are, contact us. Our state tax professionals work with you so you can make the right choice for your business.

Option 2: Voluntary Disclosure Agreement (VDA)

Maryland's lookback period: The standard lookback period is four years.

In many situations, voluntary disclosures are a valuable tool to reduce extended periods of past exposure.

The voluntary disclosure limits the lookback period to four years. So, if you should have collected sales tax over the past ten years but did not, you may benefit from doing a VDA.

A VDA may be a good option for you if:

- You established nexus more than 3 or 4 years ago.

- You have a sales tax collected but not remitted issue.

- The sales tax penalty savings is MORE than the professional fees charged for the VDA.

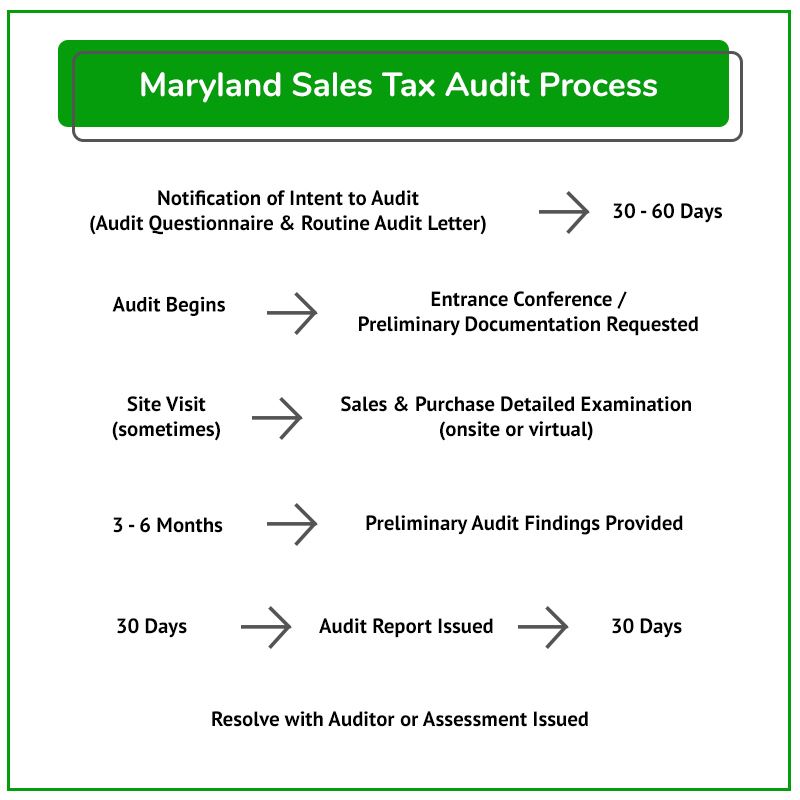

What to Expect During an Audit

The typical audit process is shown in this flowchart. Detailed guidance for each Maryland audit process stage follows in the sections below.

Maryland regularly audits businesses required to charge, collect, and remit various taxes in the State. Many audits begin with a call from a Comptroller's Office of Maryland sales tax auditor. After the call, your business will receive a Notification of Intent to Audit. This notification confirms that you were lucky enough to be chosen for a Maryland sales tax audit.

A Notice of Determination stating the reason for the assessment and the amount will be sent to you by the Tax Commissioner within 12 months from the commencement of the audit.

It is good to start with getting a state and local tax professional involved to prepare for the audit.

I received a Maryland Sales Tax Audit Notice. What Should I Do?

Businesses that receive a sales tax audit notice need to consider the following questions:

- If you do not have sales tax audit experience, how can you trust that the State's auditor abides by the rules and follows proper procedures?

- How will you know when to provide documents or when to push back?

- Do you thoroughly understand your sales and use tax areas of exposure?

- Controlling the audit is paramount to limiting exposure and shaping the results. Are you confident in doing that on your own?

Unless you can confidently answer these questions, hiring a professional is most likely to be the best option.

Contact us to learn how our sales tax professionals can give you the peace of mind and confidence you will need during your audit.

Visit our resource pages for more information to help you make critical decisions during your Maryland sales and use tax audit.

The Audit Overview & Selection Process

Statute of Limitations Extensions & Issues

Managing the Sales Tax Auditor

What to Expect from a Maryland Sales Tax Auditor

Here is a summary of the general audit process:

- The auditor will conduct pre-audit research.

- The auditor will often schedule and perform an entrance conference.

- The auditor will request records (many of which the auditor is not entitled to and does not need)

Once the auditor receives the necessary records, they will compare your Maryland sales and use tax returns to your federal income tax returns or bank statements to determine whether you reported all applicable or gross sales on your Maryland sales tax return(s).

NOTE: A slight error in how the tax was charged on even a single type of transaction can add up to a significant sales tax liability.

Once the auditor is confident all sales are accounted for, they will:

- Review your exempt and out-of-state sales.

- Conduct a use tax audit – the auditor will request accounts documents to ensure you paid use tax on applicable purchases.

Common areas audited include:

- Advertising Expense

- Auto & Truck Expense

- Repair and Maintenance

- Office Expense

- Miscellaneous Expense

- Supplies

- Equipment

If a business buys an item online and does not pay use tax, the business is still obligated to remit the tax to Maryland. Believing otherwise often leads to shocking results for the unsuspecting taxpayer during an audit. Here is more information on Maryland Use Tax.

If you have questions about your situation, contact us to discuss it with one of our tax professionals.

After the Audit – Understand and Defend Your Businesses Rights

Upon completion of the audit, there is usually an exit conference with the auditor. The auditor will produce an audit report with corresponding work papers to support the Maryland sales and use tax assessment.

It is advisable to have a sales tax professional present during this meeting. This is your first opportunity to see the auditor's findings. You will likely want to push back on areas where they have overstepped their bounds or misapplied Maryland's sales tax laws.

It is best to hold off on agreeing to the sales tax assessment until a sales tax professional has reviewed it for issues that should be challenged.

| Many businesses wind up drastically overpaying the State because the business owner or in-house accounting personnel were not well versed in the sales tax laws that, if challenged, could have reduced their sales tax liability. |

In the following sections, we will cover the process of challenging a Maryland sales tax audit assessment.

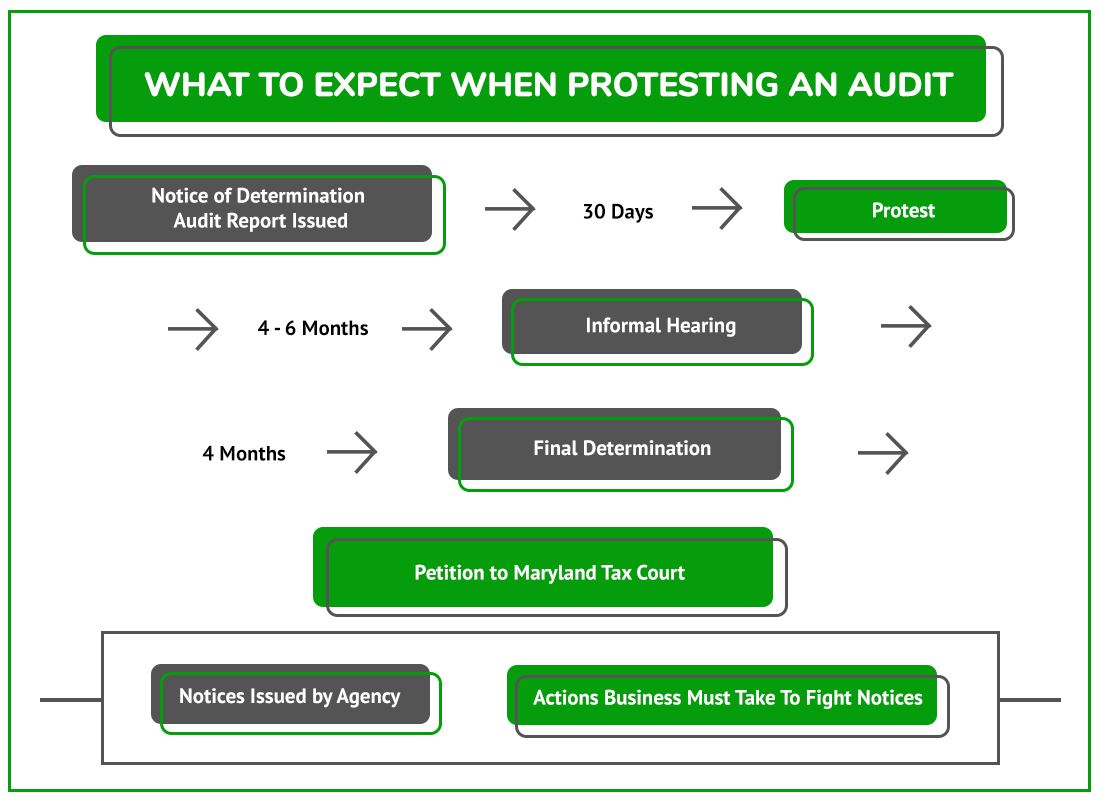

Contesting Audit Findings with the Auditor

Maryland Sales Tax Audit Protest Process Flow Chart

NOTE: If the deadlines are missed, it can be tough to get the case reopened.

After an audit, the auditor will issue a Notice of Determination (AKA the audit report). It is essential to review and understand its implications carefully.

The audit report:

- Details of the auditor's findings

- Describes any proposed audit adjustments

- Shows the amount of tax, interest, and penalty due

If you disagree with the proposed changes, you may request an informal conference with the auditor. You must request an informal meeting and attempt to resolve the case with the auditor.

Audit Closing Conference

The taxpayer has an abbreviated period to contest the findings with the auditor. Any issues with the results are handled as follows:

1. Issues related to exemptions, proof of tax paid, and calculations are worth addressing with the auditor.

2. Legal interpretations of sales tax law are often not resolvable at this stage.

After this conference, the auditor will adjust the audit assessment, and a Notice of Determination will be issued.

If you cannot resolve this with the auditor, the next step is to appeal/protest the issue.

Appeal/Protest with Comptroller’s Office of Maryland

An informal hearing is the first step in the appeal process with the Comptroller’s Office.

Protest Rights and Audit Finding Confirmation

When you receive an assessment notice, you have 30 days to respond with a request for a hearing to dispute the liability. If the assessment is not appealed, it will become final, and the liability becomes subject to the collection process.

If you have received a Notice of Assessment and have not talked to someone experienced in Maryland State tax, now is the time. Do it before these deadlines are missed.

Informal Hearing with The Comptroller’s Office of Maryland

Once you file a written appeal, you will receive a Notice of Hearing advising you of the date and time of the hearing. If you believe that the circumstances of your case are straightforward or based on a lack of documentation, including missing information with your appeal will help to resolve your dispute without the need for an in-person hearing.

The hearing is often recorded between you and the Comptroller before a hearing officer. During the informal hearing, the officer will hear arguments and examine documents provided by the Taxpayer. The officer will often question the Comptroller and the taxpayer or their representative, attorney, or other professional. Following the hearing, a final determination is issued by the Comptroller's office.

Final Decision

The Commissioner must issue a decision no later than 30 days from the conclusion of the hearing.

You may appeal the Commissioner's decision to the Maryland District Court. For additional information, see Appeals.

Our team has handled hundreds of administrative court cases. It can help your company receive the resolution you are entitled to. Contact us today.

Settling a Maryland Sales Tax Liability

After any critical notices are issued, settling your Maryland sales tax case with the Comptroller’s Office of Maryland is possible by filing a Maryland Offer in Compromise. The business must meet specific criteria to qualify, but you can get better results negotiating here than with the auditor. However, knowing a fair settlement from an unreasonable settlement will be challenging without experience and knowledge of Maryland tax laws.

DO NOT attempt to negotiate a settlement without an experienced Maryland state and local tax lawyer or other professional.

Contest a Maryland Jeopardy Assessment

Maryland may issue a Notice of Jeopardy Determination in certain situations.

The jeopardy assessment gives the Comptroller’s Office of Maryland the right to try to collect immediately.

Due to the jeopardy nature, the taxpayer only has a brief time to contest the assessment and must place a security deposit to fight the issue.

Maryland Tax Court

Suppose you cannot resolve the case within the agency. There is still one chance to fight your Maryland sales tax assessment - the Maryland Tax Court. The Maryland Tax Court is an independent agency specializing in hearing tax disputes against the Comptroller's office. The goal of the Tax Court is to provide an independent review and resolution for taxpayers. Like a typical court, the cases are heard by a Tax Court Judge.

Although it is not technically a court, Maryland Tax Court behaves much like a regular judicial court. Once the petition has been filed, there is a period of discovery. Following discovery, a proceeding is scheduled, at which the judge hears testimony from witnesses and receives evidence. Following the hearing, the judge renders a decision.

Due to its court-like nature, it is strongly recommended to have a sales tax attorney or professional on your side during a Tax Court appeal. It is critical to get evidence admitted to help the judge rule in your favor and develop the record if further appeals are necessary. This stage also provides a substantial opportunity for Taxpayer's to get a favorable settlement instead of going to trial/hearing.

If the State or the taxpayer disagrees with the decision, the case can be appealed to a judicial court.

Other Maryland Sales Tax Resources

The Comptroller’s Office of Maryland Sales Tax Website

Marylandtaxes.gov | Business Taxpayers

Taxpayer Rights (marylandtaxes.gov)

Sales Tax FAQ (marylandtaxes.gov)

If you have received a Notice of Assessment and have not talked to someone experienced in Maryland State tax, now is the time. Do it before these deadlines are missed.

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.