Colorado Sales Tax & Audit Guide

Your Answers to Common Colorado Sales Tax Questions.

- When Should I get a Colorado sales tax license?

- Should I be collecting or paying Colorado use tax?

- What do I do if I should have been collecting but haven't?

- What steps could I take after receiving an audit notice?

- Guidance on fighting a sales tax assessment in Colorado.

When Should Colorado Retailers Get a Sales and Use Tax License?

A retailer who maintains a physical place of business in Colorado directly, indirectly, or by a subsidiary must obtain a retail sales tax license regardless of how much they sell.

According to the Colorado Department of Revenue, physical presence in Colorado could include the following for sales tax registration purposes:

- Using an office space, warehouse, storage facility, or other real property.

- Having agents conduct business on your behalf in Colorado.

- Assembling, installing, servicing, or repairing products in Colorado.

- Owning, renting, or leasing real property or tangible personal property in Colorado, including a computer server or software to solicit orders for taxable items.

- Delivering goods to Colorado customers using your company-owned or leased truck.

- Maintaining inventory in Colorado using a third-party fulfillment service, such as Fulfilled by Amazon (“FBA”).

An out-of-state retailer (or one with no physical presence) must apply for a Colorado Sales Tax License and collect Colorado sales tax if:

- Your gross sales, delivered in Colorado, including exempt sales, reached $100,000 or more in either the previous or current calendar year. Retailers must start collecting within 90 days of the first day of the first month after the retailer hits the $100,000 aggregate sale threshold.

Any retailer who does not maintain a physical location in Colorado is exempted from state sales tax licensing and collection requirements if:

- the total annual retail sales in both the current and previous calendar years were less than $100,000.

How is the $100,000 gross revenue threshold calculated?

All Colorado retail sales are included for the purpose of calculating the $100,000 threshold, whether those sales are subject to Colorado tax or not.

Marketplace Sellers

If your business sells through Amazon or a similar marketplace provider, you may not have to collect sales and use tax on those sales. Specifically, if the marketplace provider certifies that they are collecting and reporting sales tax, Colorado should hold them responsible for compliance related to your marketplace sales through them.

However, such sales may still count towards your total sales threshold. You'll still need to collect tax on sales made directly through your website or any other marketplaces that don't collect sales tax on your behalf.

See this Marketplace Guide for Colorado Sales Tax for more information.

Which Sales are Subject to Colorado Sales Tax?

General Transactions

Colorado requires the collection of sales tax on certain retail sales of tangible personal property and services except when such sales qualify for an exemption. Common examples of taxable retail transactions in Colorado could include:

- Prepared foods and drinks sold in restaurants

- Merchandise

- Household goods

- Motor vehicles

- Digital goods (e.g., music, movies, eBooks)

- Any other tangible property you can possess and exchange.

Common Exemptions from Colorado Sales and Use Tax

Colorado exempts sales tax on the purchase of certain items across several categories.

You can find guidance from the Department of Revenue on tax-exempt items here:

- Food bought for consumption at home (i.e., packaged, unprepared food you buy at the grocery store)

- Agriculture supplies (e.g., seeds, plants, pesticides, farm equipment)

- Machinery and tools for manufacturing

- Coins and precious metal bullion

- Medical equipment

- Medicine

- Residential energy (e.g., natural gas or electricity)

Services

Sales of services are generally not subject to Colorado sales tax, except for the following:

- Commercial gas and electric services (i.e., not for residential purposes)

- Intrastate telephone and telegraph services

- Nontaxable services provided as part of a transaction involving a taxable sale of tangible personal property (depending on the facts)

Software

Colorado sales tax applies to any sale of computer software where all the following conditions are met:

- You prepackage the software for repeated sale or license.

- The sale of software is subject to a “tear-open nonnegotiable license” contained in the packaging (i.e., not signed by the parties).

- You deliver the software in a physical medium such as a disk, tape, or card.

Software as a Service (SaaS)

Sales of computer software are non-taxable when the software is delivered by any of the following methods:

- Application service providers: "Application service provider" or "ASP" retains custody over the software but allows purchasers to use the services fulfilled through the software via the internet (i.e., Software as a Service “SaaS”).

- Electronic delivery: No delivery takes place through a tangible medium and the purchaser receives the software remotely to their computer.

- “Load and leave" delivery: The transfer of software takes place via a tangible medium (e.g., a CD or USB stick) but the purchaser does not retain possession of the medium after loading the software.

Shipping & Handling

Shipping charges are exempt if "separable from the purchase and separately stated" on the invoice (See FAQ #12 from the CDOR).

In other words, if the charges are added after the property is offered for sale and the purchaser can select the shipping method, these charges are exempt. Shipping charges for non-taxable items are also exempt.

Colorado Delivery Fees

As of July 1, 2022, retailers who make retail deliveries must collect and remit a delivery fee for each taxable sale of tangible personal property delivered by motor vehicle to a purchaser at a location within Colorado.

- This delivery fee also applies to deliveries by motor vehicle from another state to a site in Colorado.

- A motor vehicle is any self-propelled vehicle designed primarily for travel on the public roads, is generally and commonly used to transport people and property over the public highways or roads; or a low-speed electric vehicle.

- If every item in a retail sale is exempt from sales tax, the delivery is also exempt from the retail delivery fee.

- Conversely, if one or more items in the transaction are subject to sales tax, you must collect the retail delivery fee.

- The total fees must be shown on the receipt or invoice as a separate item called "retail delivery fees."

Industry-Specific Guidance

Sales tax rules are not always so simple thanks to special laws, caveats, and application of broader tax structures to unique industries. The Colorado Division of Taxation provides some specific guidance for the following industries:

- Agriculture - Sales & Use Tax Topics

- Aircraft and Aircraft Parts - FYI Sales 85

- Beetle Wood Products - Sales & Use Tax Topics

- Bingo Equipment - FYI Sales 65

- Charitable Organizations - Sales & Use Tax Topics

- Coins and Precious Metal Bullion - FYI Sales 60

- Computer Software - Sales & Use Tax Topics

- Construction Contractors - FYI Sales 6

- Dining Establishments - Sales & Use Tax Topics

- Direct Pay Permit for Colorado Sales Tax - FYI Sales 78

- Food and Related Items - FYI Sales 4

- Gasoline and Special Fuel Subject to Sales Tax - FYI Sales 57

- Governmental Entities - Sales & Use Tax Topics

- Leased Departments Within Stores - FYI Sales 67

- Leases - Sales & Use Tax Topics

- Low-Emitting Heavy Vehicles - FYI Sales 91

- Manufacturing - Sales & Use Tax Topics

- Marijuana Sales Tax - FYI Sales 93

- Marketplace Facilitators - Sales & Use Tax Topics

- Medicine and Medical Equipment - Sales & Use Tax Topics

- Motor Vehicle Daily Rental Fee (under review) - FYI General 19

- Motor Vehicles - Sales & Use Tax Topics

- Penalties and Interest - General 11

- Prefabricated Housing - Sales & Use Tax Topics

- Refund for Vehicles Used in Interstate Commerce - FYI Sales 88

- Renewable Energy Components - Sales & Use Tax Topics (Replaced FYI Sales 83)

- Residential Energy Usage - FYI Sales 66

- Rooms and Accommodations - Sales & Use Tax Topics

- Sales by Schools and School Organizations - FYI Sales 86

- Sales/Use Tax Exemption for Affordable Housing Projects - FYI Sales 95

- Telephone and Telecommunications - FYI Sales 80

- Telephone Charges by Hotels/Motels - FYI Sales 61

- Vending Machines - FYI Sales 59

Determining Local Sales Tax Rates in Colorado

The state sales tax rate in Colorado is 2.900%. You can use this tax lookup tool to find information about local taxes in the state of Colorado.

County and city sales taxes collected by the state are administered in the same manner as state sales tax. If the sale is subject to state sales tax, it is also subject to state-collected local sales tax.

Under Colorado law, a retail sale is usually sourced to the location where the purchaser takes possession of the purchased property. This is known as destination sourcing and applies to determining applicable local rates.

The Colorado Department of Revenue generally collects sales tax on behalf of cities, counties, and special districts. Such jurisdictions are referred to as "state collected".

All Colorado counties that impose a sales tax are state collected, except Denver County and Broomfield County. These are "Home-rule" localities that have elected to administer their own sales and use taxes. They are also referred to as "self-collected".

For more information about local sales tax, refer to Part 8 of the Colorado Sales Tax Guide

Local Sales and Use Tax Tables

The following tax table shows the total tax rate in each Colorado county.

What Happens When You Fail to Collect or Pay Sales Tax in Colorado?

If your business hasn’t been collecting or remitting Colorado sales and use tax when it should have, then you have a couple options for compliance moving forward. You can either pay the outstanding tax liability or consider Colorado’s voluntary disclosure program. Each option comes with pros and cons that will make one better than the other depending on your situation.

Option 1: Register to Pay Back Taxes, Penalties, and Interest.

Other sales tax professionals may be quick to recommend participating in Colorado’s voluntary disclosure, but this is not always the most cost-effective approach in our experience. Sometimes, you are better off just paying the tax you owe in full.

When to consider registration and payment:

- If you established nexus less than 3 years ago.

- The sales tax penalty is LESS than the professional fees needed to facilitate the disclosure

- Your business has not collected Colorado sales tax.

Note: Registering won’t negate your past liabilities so it’s critical to know your outstanding balance when forgoing participation in a VDA.

If you lack clarity on your past liabilities, contact us. Our state tax professionals could help you understand the amount of Colorado sales tax you may owe.

Option 2: Voluntary Disclosure Agreement (VDA)

Colorado's lookback period: The standard lookback term for a voluntary disclosure agreement is three years for sales and use tax. This means the CDOR will generally limit the scope of your liability to the past three years and waive rights to collect sales tax from before then.

In many situations, voluntary disclosures are a valuable tool to reduce extended periods of past exposure.

A VDA may be a good option for you if:

- You established nexus more than 3 years ago.

- The sales tax penalty savings is MORE than the professional fees charged for the VDA.

- You collected Colorado sales tax but did not properly remit it to the DOR.

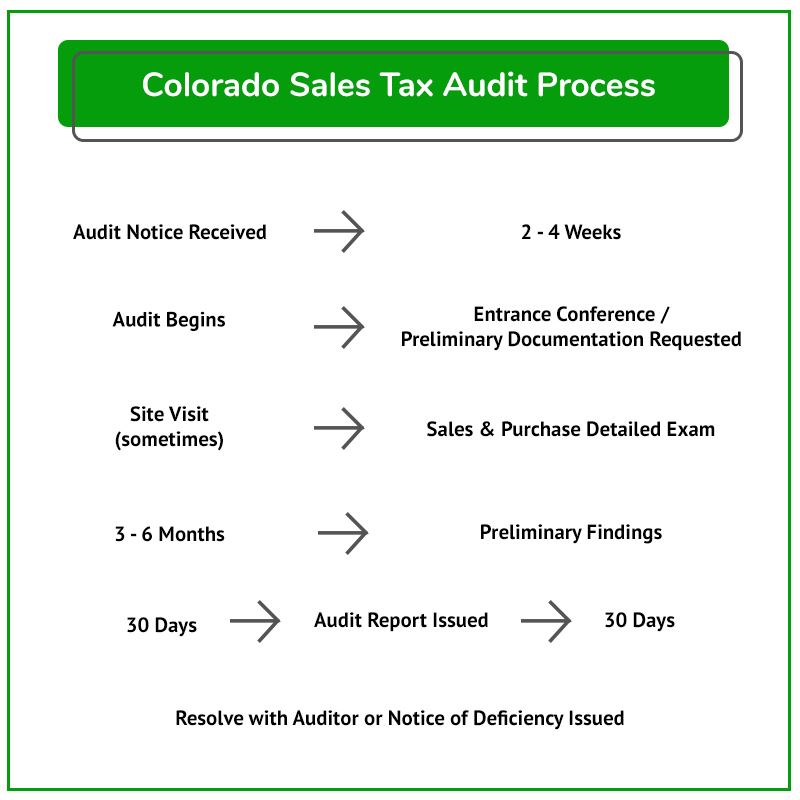

What Businesses Might Expect During a Colorado Sales Tax Audit

Consider the general process for a sales tax audit in Colorado illustrated through the flowchart below, which includes detailed guidance for each stage of the audit process.

Colorado Sales Tax Audit Protest Process Flow Chart

The Colorado Department of Revenue regularly audits Colorado businesses when they fail to file sales tax returns or their SUTRs are inconsistent with other data in the possession of the state. An audit generally begins when you receive that dreaded preliminary audit notice.

If the Colorado Department of Revenue determines the correct amount of tax has not been paid, your business will receive a Notice of Deficiency.

I Received a Colorado Sales Tax Audit Notice. What Should I Do Next?

Businesses that receive a sales tax audit notice need to consider the following questions when considering next steps:

- If you don’t have sales tax audit experience, how can you trust that the state's auditor abides by the rules and follows proper procedures?

- How will you know when to cooperate with document requests versus when to challenge the auditor?

- Do you have a good understanding of your overall sales and use tax exposure in Colorado?

- Controlling the audit is paramount to limiting exposure and shaping the results to accurately reflect your sales tax position. Are you confident in doing that on your own?

Unless you can confidently answer these questions, hiring a professional is most likely to be of some value. Contact us to learn how our sales tax professionals can give you the peace of mind and confidence you’ll need during the audit process.

Visit our resource pages for more information to help you make critical decisions during your Connecticut sales and use tax audit.

- The Audit Overview & Selection Process

- The General Audit Process

- Statute of Limitations Extensions & Issues

- Managing the Sales Tax Auditor

What to Expect from a Colorado Sales Tax Auditor

In addition to the standard audit procedures outlined below, Colorado has also enacted a policy regarding retail transactions where an audit finds a retailer hadn't collected sales tax from another retailer currently being audited. If you are doing business in Colorado, it may be worth reviewing.

If you have questions about your situation, contact us to discuss it with one of our tax professionals.

For now, here is the summary of the general audit process:

- The auditor will conduct pre-audit research.

- The auditor will often schedule and perform an entrance conference.

- The auditor will request records (many of which the auditor does not have a right to review)

Once the auditor receives the necessary records, they will compare your Colorado sales and use tax returns to your federal income tax returns or bank statements to determine whether you reported all applicable or gross sales on your Colorado sales tax return(s).

NOTE: A slight error in how the tax was charged on even a single type of transaction can add up to a significant sales tax liability.

Once the auditor is confident all sales are accounted for, they will:

- Review your exempt and out-of-state sales.

- Conduct a use tax audit – the auditor will request documents of accounts to make sure use tax was paid adequately on applicable purchases.

Common business expense categories audited for use tax payment could include:

- Advertising Expense

- Auto & Truck Expense

- Repair and Maintenance

- Office Expense

- Miscellaneous Expense

- Supplies

- Equipment

Note: If a business buys an item online without paying sales tax, the business may still be obligated to remit use tax to Colorado.

After the Audit – Understand and Defend Your Businesses Rights

The auditor will likely hold another informal conference after completing the audit and will share the findings via report with you. This is your first opportunity to push back on areas where they have strayed from procedure, made errors in calculations, or misapplied Colorado's sales tax laws. It is advisable to have a sales tax professional present during this meeting.

It's best to hold off on agreeing to anything until a sales tax professional has reviewed it for issues that should be challenged.

NOTE: A slight error in how the tax was charged on even a single type of transaction can add up to a significant sales tax liability.

Unless you agree with and choose to pay the state's estimated total due, a Notice of Deficiency will follow. Receipt of the notice will require you to respond by either:

- paying the amount shown on the deficiency; or

- filing a protest or request for a hearing.

Under Colorado law, a notice of deficiency can be issued no later than three years after the return was filed or three years after the return was due, whichever is later.

However, for taxpayers who do not file a required return, or in the case of a false or fraudulent return with the intent to evade tax, there is no limit on the time for the tax department to estimate the tax due, along with any applicable penalties and interest, and issue a Notice of Deficiency.

It is wise to start by getting a state and local tax professional involved to prepare for the audit.

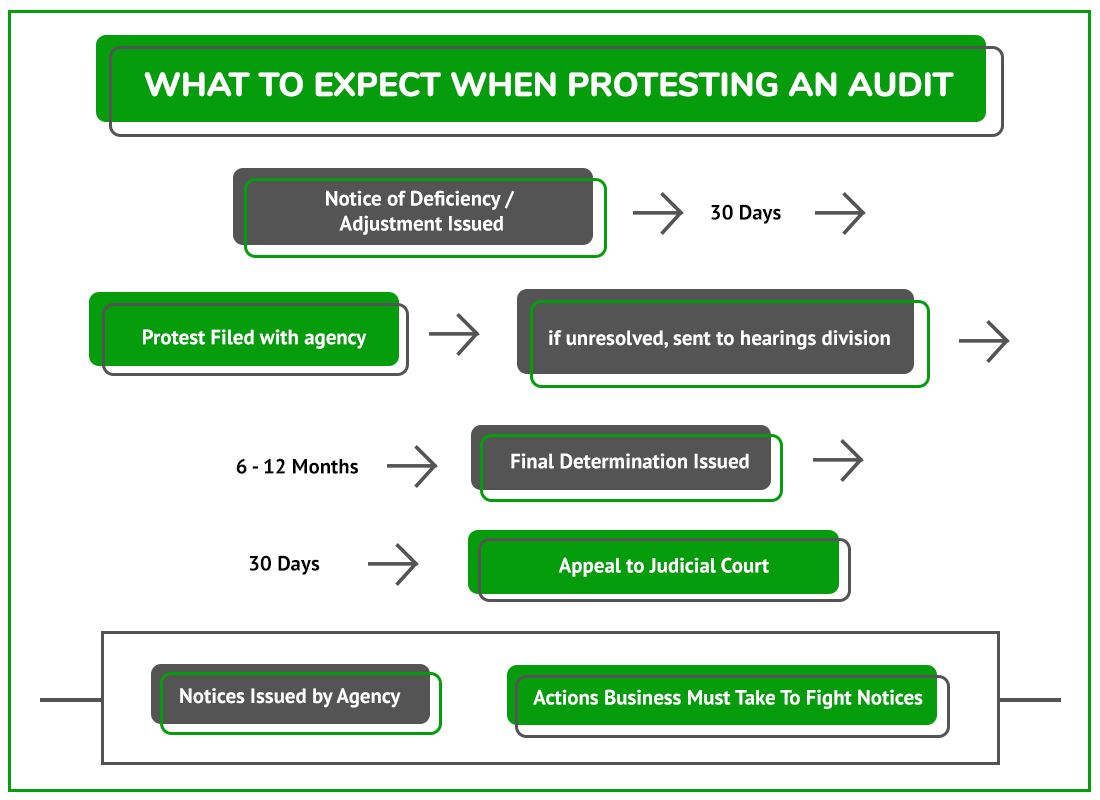

I Received a Colorado Sales Tax Notice of Deficiency. What Should I Do?

After receiving a Notice of Deficiency for Colorado sales and use tax, businesses have two options moving forward. You can agree to pay the amount of the deficiency, or you could further protest or appeal the notice. Deciding between the two will likely depend on the amount of errors with the audit or deficiency notice compared with the administrative cost of pursuing a protest.

Protesting Audit Findings with the Auditor

Like the audit process, the protest of a Colorado Notice of Deficiency or Assessment has its own steps and timelines that business owners should consider.

Colorado Sales Tax Audit Protest Process Flow Chart

Appeal/Protest with The Colorado Department of Revenue

Under Colorado law, a formal administrative hearing before the Director of Revenue must be allowed for taxpayers who timely dispute a notice of deficiency or rejection of refund claim.

Taxpayers who receive a notice of deficiency or notice of refund rejection may submit a written protest and request a hearing to dispute the notice within 30 days of the date of the notice.

Your protest will need to provide the following information to the Colorado Department of Revenue:

- Identifying information (e.g., your name, address, and account number)

- The tax period(s) that are the subject of the protest (usually the audited period)

- A statement of the type and amount of tax you are protesting

- A summary statement of findings with which the retailer disagrees and the grounds upon which the retailer relies to show the tax is not due.

- The retailer must sign the protest or request for a hearing.

- The application for a hearing must be made to the Executive Director of the CDOR. However, it should be mailed to the reviewer's attention whose name and address appear on the notice of deficiency or rejection of refund claim.

You can be denied valid standing in an appeal to the courts if a valid protest is not timely filed and this can allow the Department to begin collection procedures.

All protests will be reviewed by the originating section (i.e., the sales tax office) for factual matters.

If they cannot resolve the protest, the protest will go to the Tax Conferee Section for further review.

Though we don't recommend doing this without first speaking with a tax professional at any time during the audit process, the Colorado Department of Revenue allows taxpayers to request that the Executive Director of the Colorado Department of Revenue reconsider the deficiency without a hearing.

If you have received a Notice of Deficiency and haven't talked to someone experienced in Colorado State and Local tax, now is the time. Do it today, before the deadline has passed.

What to Expect from a Colorado Tax Conferee

Upon receipt of a request for a hearing, the Department's Tax Conferee Section will assign the case to a Tax Conferee.

The Tax Conferee will:

- Review your written protest before the scheduling of any formal hearing.

- Review your exempt and out-of-state sales.

- Conduct a use tax audit – the auditor will request documents of accounts to make sure use tax was paid adequately on applicable purchases.

- Accept or reject the suggested changes listed in your protest. As a part of this process, the Conferee may schedule one or more informal conferences to do the following:

- Discuss the administrative hearing procedures,

- Clarify the relevant facts, issues, and law; and

- Allow the submission of additional evidence in support of the protest, and, if possible, to settle the matters in dispute.

The informal conference does not waive the taxpayer's right to a formal administrative hearing.

After the Audit (Tax Conferee Review) – Understand and Defend Your Businesses Rights

If the Tax Conferee cannot resolve the protest, the case will be forwarded to the Hearing Division of the Department, and an administrative (formal) hearing will be scheduled.

The Executive Director/ Deputy Director must notify you in writing of the time, date, and place for the hearing at least 30 days before the hearing date.

Administrative Hearing

The hearing will be held before the Executive Director/Deputy Director, or another designated employee within the Department of Revenue who will be selected by the Executive Director to hear your dispute. Under Colorado law, partnership and corporate taxpayers must be represented by counsel.

Due to the nature of the administrative hearing (it is very similar to a court hearing),we strongly recommend having an experienced representative at this stage of the audit process.

Our team has handled hundreds of administrative court cases. We can help your company receive the resolution you are entitled to. Get in touch with us today.

Final Decision

After reviewing the evidence and arguments, or the brief and written materials submitted instead of a hearing, the Executive Director/Deputy Director will make a final determination within 60 days.

The deadline for a final determination may be extended in sixty-day increments. The Executive Director could modify the tax, penalties, and interest disputed at the hearing or approve a refund if necessary. All these decisions will be found in the Colorado Department of Revenue’s issuance of a Final Decision.

Appeal to Judicial Court

If the CDOR’s Final Decision is not to your liking and contains issues worth challenging, you could further appeal to a Colorado judicial district court. The district court could affirm, modify, or reverse the determination of the Executive Director. The district court's decision appears as a judgment, as in other civil cases, against the taxpayer or the Executive Director.

Settling a Colorado Sales Tax Liability

After any one of the critical notices is issued, it's possible to settle your Colorado sales tax case with the Colorado Department of Revenue by filing an Offer in Compromise. However, to qualify, the business must meet specific criteria. Often, you can get better results negotiating here than with the auditor.

Without experience and knowledge of Colorado tax laws, knowing a fair settlement from an unreasonable one will be challenging.

DO NOT attempt to negotiate a settlement without an experienced Colorado state and local tax lawyer or other professional.

Contest a Colorado Jeopardy Assessment

Colorado may issue a Notice of Jeopardy Determination in certain situations.

The jeopardy assessment gives the Colorado Department of Revenue the right to try to collect immediately.

You must make a security for payment satisfactory to the executive director to stay collections. Due to the jeopardy nature, the taxpayer only has 20 days to contest the assessment and must place a security deposit to fight the issue.

Colorado Court of Appeals

If you or the Department of Revenue is not satisfied with the decision by the district court, either or both may appeal further to the Colorado Court of Appeals or the Colorado Supreme Court. To appeal the district court's decision, the taxpayer must first satisfy a bond requirement.

After the above appeals are exhausted, the taxpayer or the Department of Revenue must pay any amount ordered in the court’s judgment.

Additional Colorado Sales Tax Resources

Colorado Department of Revenue Sales Tax Website

Colorado Sales and Use Tax Guidance Publications

Reviews

-

"Jerry Provided Calming, Clear Guidance"

I can't say enough about Jerry and STH. We were in a bit of a panic re reaching nexus levels and dealing with reseller tax ...

- Mike L. -

"My Entire Experience Was Superior"

My entire experience from intake to resolution with Sales Tax Helper was superior. '11' on a scale of 1-10! Initial meeting ...

- Tim N. -

"Prompt, Courteous & Helpful!"

I sincerely am grateful for the prompt, courteous, and helpful that has been offered me by Sales Tax Helper. My agent, Alex ...

- Carol M. -

"Professional and Very Communicative"

When my business needed guidance with sales and use tax, I reached out to Sales Tax Helper through their website and received ...

- Pierce L. -

"They Are Experts in Their Field"

Jerry & Alex are excellent at what they do. They helped me navigate some very difficult and stressful situations. They’re ...

- Greg M. -

"Excellent Team to Work With!"

The team at Sales Tax Helper was excellent to work with. I had a complex business sales tax challenge that they methodically ...

- Mike M. -

"Always Provide Accurate & Prompt Responses"

Alex and Jerry always provide very accurate and prompt responses to my inquiries regarding the sales tax. They also bring ...

- Lukas P. -

"Jerry is the best!"

Jerry is the best! I made the mistake thinking I could deal with the use tax auditor on my own not realizing that I would be ...

- Gary O.